Table of Contents

- Understanding the Home Appraisal Process

- What Makes Appraising Portland Homes Different?

- First Impressions Count: Maximizing Your Home’s Curb Appeal

- Inside Matters: Addressing Interior Condition and Minor Repairs

- Non-Negotiable: Meeting Oregon’s Health and Safety Standards

- The Paper Trail: Essential Documentation for a Higher Appraisal

- Smart Investments: What Actually Adds Value Before an Appraisal?

- Key Takeaways

When selling your Portland home, few moments are as critical as the appraisal. This professional evaluation doesn’t just determine your home’s market value—it can make or break your entire transaction. In fact, appraisal-related issues were responsible for terminating approximately 12% of real estate contracts in May 2024. For Portland sellers, where the median home price reached $575,000 in May 2024, even a modest appraisal gap can represent tens of thousands of dollars at stake. The good news? You have more control over your appraisal outcome than you might think. While you can’t change market conditions or dictate which comparable properties (“comps”) an appraiser selects, you can ensure your home is presented in its absolute best light—both physically and on paper. This comprehensive guide will walk you through everything you need to know about the appraisal process in Portland’s unique real estate market. You’ll learn exactly what appraisers evaluate, why Portland homes have specific considerations (from ADUs to seismic safety requirements), and most importantly, a detailed action plan to prepare your property for appraisal day. Whether you’re selling a historic Craftsman in Ladd’s Addition or a modern condo in the Pearl District, this guide will help you maximize your home’s appraised value and ensure a smooth path to closing.

Understanding the Home Appraisal Process

Before you can prepare effectively, you need to understand what appraisers are actually looking for and how they determine your home’s value.

The Appraiser’s Mission and Standards

Licensed appraisers in Oregon follow the Uniform Standards of Professional Appraisal Practice (USPAP), ensuring objective, professional evaluations. Their job is to provide lenders with an unbiased opinion of your property’s fair market value—protecting both the buyer and the lending institution from overpaying for a property.

The Uniform Residential Appraisal Report (URAR)

Most single-family home appraisals use Fannie Mae Form 1004, known as the URAR. This standardized form guides appraisers through a comprehensive property evaluation, from foundation to roof, ensuring consistency across all residential appraisals nationwide.

What Appraisers Examine

During the inspection, appraisers conduct a thorough evaluation that includes:

Site characteristics: Lot size, topography, zoning (including Portland’s Residential Infill Project zoning), and utility access all factor into your home’s valuation.

Exterior condition: The appraiser examines your foundation, siding, roof, windows, doors, porches, and overall curb appeal. Any visible damage or deferred maintenance is documented and can impact your final valuation.

Interior features: Room count, layout, flooring, finishes, and the critical Gross Living Area (GLA) measurement are carefully recorded. It’s important to note that finished basements, while valuable, are typically excluded from GLA calculations and assessed separately.

Systems: The age, condition, and functionality of your HVAC, electrical, and plumbing systems are evaluated. Well-maintained systems signal a well-cared-for home overall.

Special features: Garages, finished basements, ADUs, and upgrades like new windows or energy-efficient improvements all contribute to your home’s value when properly documented.

Condition and Quality Ratings

Appraisers assign standardized ratings (C1-C6 for condition, Q1-Q6 for quality) that allow objective comparisons between your home and comparable sales. A C3 rating (“well maintained”) versus a C4 (“adequately maintained with minor deferred maintenance”) can significantly impact your valuation—sometimes by tens of thousands of dollars.

Fannie Mae Property Condition Ratings:

- C1: Recently constructed, never occupied

- C2: New or like-new condition, recently renovated

- C3: Well maintained with some remodeling or updates

- C4: Adequately maintained with minor deferred maintenance

- C5: Obvious deferred maintenance needing significant repairs

- C6: Substantial damage affecting safety or structural integrity

The Three Valuation Approaches

Sales Comparison Approach: The primary method—comparing your home to recent sales of similar properties with adjustments for differences. This approach carries the most weight in residential appraisals.

Cost Approach: Calculating replacement cost minus depreciation, most relevant for new construction or unique properties.

Income Approach: Based on rental income potential, typically only for investment properties or homes with income-generating ADUs.

What Makes Appraising Portland Homes Different?

Portland’s diverse neighborhoods, progressive zoning, and specific building requirements create unique appraisal considerations that sellers must understand.

Neighborhood Diversity Matters

Portland’s distinct neighborhoods—from historic Ladd’s Addition to the modern Pearl District to suburban Beaverton—each have unique architectural styles and market values. Appraisers must find truly comparable properties within your specific micro-market, not just anywhere in the Portland Metro area. A Craftsman bungalow in Southeast Portland requires different comps than a contemporary townhome in the Pearl District.

The Age Factor

Many Portland homes were built pre-1978, which introduces specific considerations for government-backed loans (FHA/VA), particularly regarding lead-based paint. Any chipping or peeling paint becomes a mandatory repair item that can delay closing. This is a critical concern for sellers of older Portland homes and should be addressed proactively.

Portland-Specific Value Enhancers

Green certifications: Homes with Earth Advantage or LEED certification can command premium valuations. Studies show green-certified homes often sell for more than their non-certified counterparts, reflecting Portland’s environmentally-conscious market.

Transit and walkability: Portland’s transit-oriented culture means high walk scores, bike scores, and proximity to MAX Light Rail stations are quantifiable assets appraisers consider. A home within walking distance of a MAX station or in a highly walkable neighborhood carries demonstrable market value.

Energy efficiency upgrades: Documented improvements like heat pumps, high-efficiency furnaces, new vinyl windows, and solar panels typically receive positive adjustments—if properly documented with receipts and permits.

The ADU Advantage (and Challenge)

Portland’s progressive ADU zoning makes accessory dwelling units increasingly common. However, appraisers must find comparable sales with similar units to accurately assess their value contribution, which can be challenging but potentially significant to your overall valuation. A permitted, well-designed ADU can add substantial value, but unpermitted units may actually create appraisal complications.

Current Portland Market Context

As of May 2024, Portland Metro’s median sale price was $575,000, with homes selling at 100.2% of list price and spending an average of just 25 days on market. This competitive market context helps justify strong valuations—but only if your home’s condition supports it.

Portland Metro Housing Market Snapshot (May 2024):

- Median Sale Price: $575,000

- Sale-to-List Price Ratio: 100.2%

- Average Days on Market: 25 days

- New Listings: 3,369

- Pending Sales: 2,755

Your real estate agent can support the appraisal by providing the appraiser with a list of relevant, recent comparable sales that were used to determine your list price, ensuring they have the full market picture.

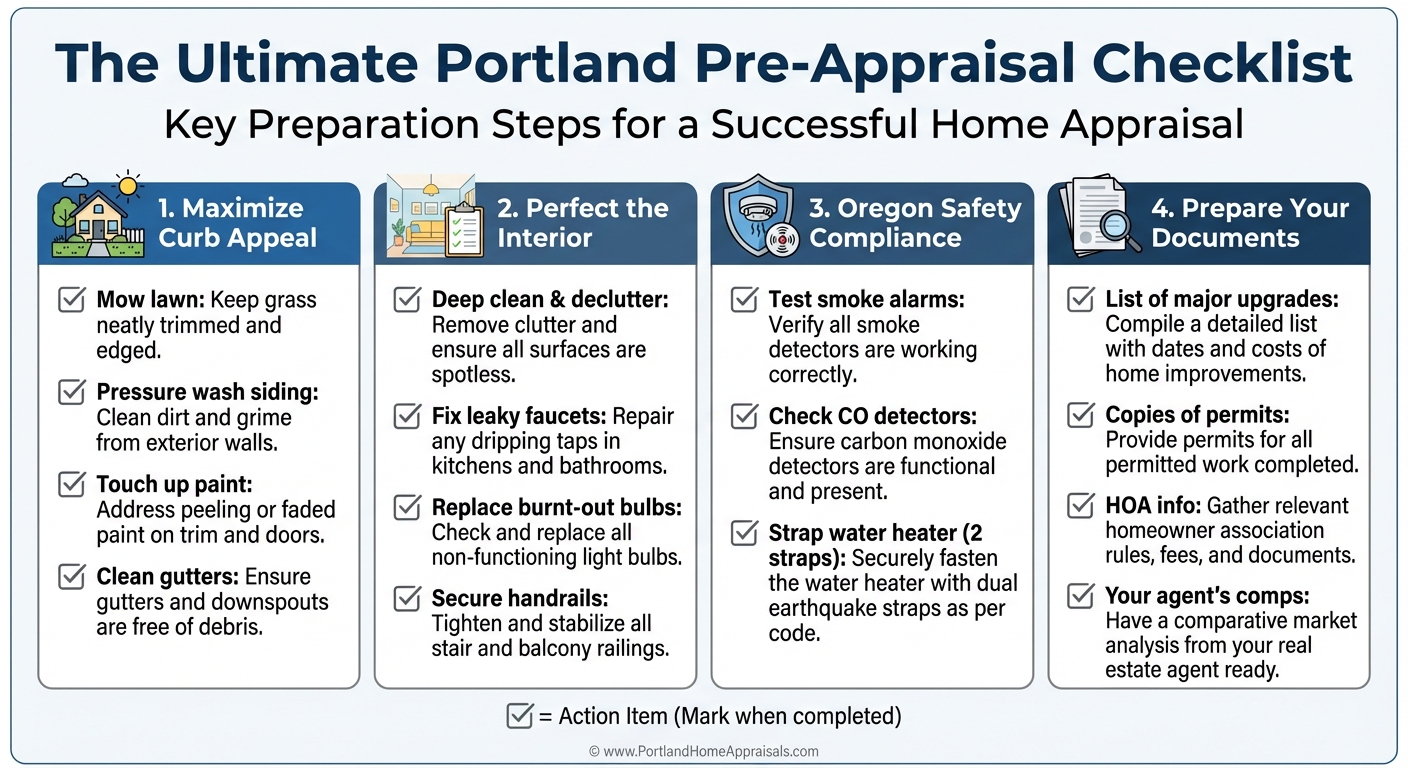

First Impressions Count: Maximizing Your Home’s Curb Appeal

The appraiser’s first impression begins the moment they arrive. Research shows good curb appeal can add up to 7% to a home’s value—that’s over $40,000 on Portland’s median-priced home.

Why Exterior Condition Matters

A well-maintained exterior signals a well-cared-for home overall, setting a positive tone for the entire inspection. Conversely, obvious neglect raises red flags about potential hidden issues. Appraisers are trained to look beyond cosmetics, but presentation matters in establishing that crucial first impression.

Your Exterior Preparation Checklist

Landscaping essentials:

- Mow the lawn and trim all overgrown shrubs

- Weed garden beds and add fresh mulch for a polished look

- Remove any dead plants or debris from the yard

- Ensure trees aren’t touching or overhanging the roof

Exterior surfaces:

- Pressure wash siding, walkways, and driveway to remove dirt, mildew, and moss

- Touch up or repaint any chipped or peeling paint—this is especially critical for pre-1978 homes with FHA/VA loans, where peeling paint is a mandatory repair due to lead paint concerns

- Clean all windows inside and out until they sparkle

Roof and gutters:

- Clean gutters and downspouts of all debris

- Note any visible roof damage (missing shingles, moss buildup) and consider repairs if significant

- Ensure proper drainage away from the foundation

Entryway presentation:

- Deep clean the front door and ensure hardware functions properly

- Make sure house numbers are clearly visible from the street

- Add a fresh doormat and consider potted plants for welcoming appeal

Hardscaping:

- Sweep all walkways and the driveway

- Repair any significant cracks or tripping hazards in concrete

- Ensure outdoor lighting fixtures are clean and functional

💡 Pro Tip:

Document your exterior improvements with before-and-after photos. If you’ve recently replaced the roof, siding, or windows, have those invoices ready for the appraiser.

Inside Matters: Addressing Interior Condition and Minor Repairs

Minor interior issues can collectively signal neglect to an appraiser, potentially dropping your condition rating from C3 to C4—and costing you thousands in appraised value.

The Power of a Deep Clean

A clean, organized home appears larger, brighter, and better maintained. This isn’t about staging for photos—appraisers are trained professionals who see past cosmetics—but cleanliness demonstrates pride of ownership and makes it easier for them to properly evaluate your home’s features.

Your Interior Preparation Checklist

Deep clean priorities:

- Declutter all rooms, especially kitchens and bathrooms

- Clean all floors, windows, and surfaces thoroughly

- Remove personal items that might distract from the home’s features

- Clean inside cabinets and closets (appraisers often open them)

Essential minor repairs:

Plumbing: Fix all leaky faucets and running toilets; check for signs of water damage or leaks under sinks

Doors and windows: Ensure all open, close, and lock properly—the appraiser will test them

Walls: Repair any holes, cracks, or significant drywall damage; touch up paint in high-traffic areas

Lighting: Replace ALL burnt-out bulbs—appraisers test every light fixture

Stairs: Secure any loose handrails (building codes generally require handrails on stairs with four or more risers)

Flooring: Repair any loose tiles, torn carpet, or damaged hardwood; consider replacing heavily worn carpet

The Paint Advantage

A fresh coat of neutral-colored paint is one of the most cost-effective ways to improve your home’s interior appearance and potentially increase your condition rating. Focus on high-impact areas like the living room, kitchen, and master bedroom.

Functionality Testing Before Appraisal Day

- Run a complete cycle on your HVAC system to ensure it heats/cools properly

- Test all major appliances (if included in the sale)

- Verify hot water heater is functioning

- Check that the garage door opener works

- Test all plumbing fixtures for proper water pressure and drainage

What NOT to Do

Don’t attempt major DIY renovations right before the appraisal. Poorly executed work can actually hurt your value. If you lack the necessary permits for past work, consult with your agent about disclosure requirements.

📊 Real-World Impact:

Consider two similar Sellwood homes under contract for $650,000. Home A, with a sticky front door, dripping faucet, and non-functional smoke detector, received a C4 rating and appraised at $635,000. Home B, which addressed these minor issues and provided documentation of recent upgrades, earned a C3 rating and appraised at $655,000—a $20,000 difference from simple preparation.

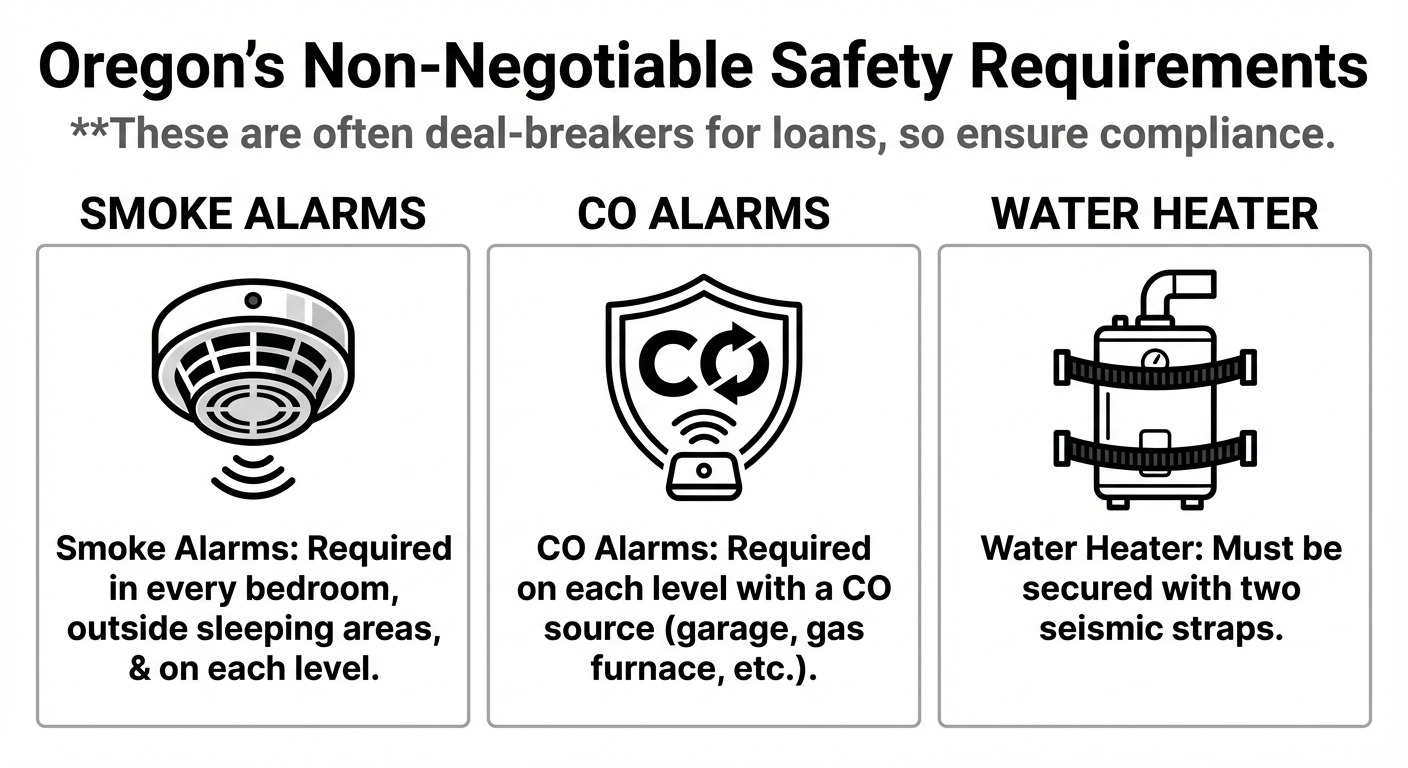

Non-Negotiable: Meeting Oregon’s Health and Safety Standards

Appraisers are required to note health and safety violations, which can halt your loan process until rectified. For Portland sellers, compliance with Oregon’s specific requirements is critical.

Why Safety Compliance Matters

Unlike cosmetic issues, health and safety violations are deal-stoppers. Lenders won’t fund loans on properties with code violations, and fixing them after the appraisal creates delays, renegotiations, and potentially lost deals.

Oregon’s Mandatory Safety Requirements

Smoke alarms (ORS 479.270):

- Required in every sleeping area (bedroom)

- Required in hallways or areas immediately outside sleeping areas

- Required on each level of the home, including basements

- All alarms must be functional—test each one before the appraisal

- For homes built or remodeled after certain dates, hardwired alarms with battery backup may be required

Carbon monoxide (CO) alarms (ORS 476.725):

- Required on each level of any home containing a CO source

- CO sources include: attached garages, gas furnaces, fireplaces, wood stoves, or any fuel-burning appliance

- Like smoke alarms, all CO detectors must be tested and functional

Water heater seismic strapping:

- Due to significant earthquake risk from the Cascadia Subduction Zone, water heaters must be properly secured

- Required: Two seismic straps—one on the top third and one on the bottom third of the tank

- This is a standard requirement for FHA, VA, and many conventional loans in the Pacific Northwest

- Improperly strapped or unstrapped water heaters are common appraisal flags

Additional FHA/VA requirements for older homes:

- Homes built before 1978: No chipping or peeling paint (lead-based paint hazard)

- Handrails on all stairs

- No broken or cracked windows

- Functional heating system capable of maintaining minimum temperatures

Ensuring Appraiser Access

- Provide clear, safe access to ALL areas: attic, crawlspace, garage, basement, and any outbuildings

- Unlock gates and doors; clear pathways

- If you have a difficult-to-access attic or crawlspace, inform your agent in advance

- Secure pets during the inspection

💡 Pro Tip:

Consider hiring a pre-listing home inspector to identify any safety or code violations before you list. Understanding what they look for and addressing issues proactively prevents appraisal surprises.

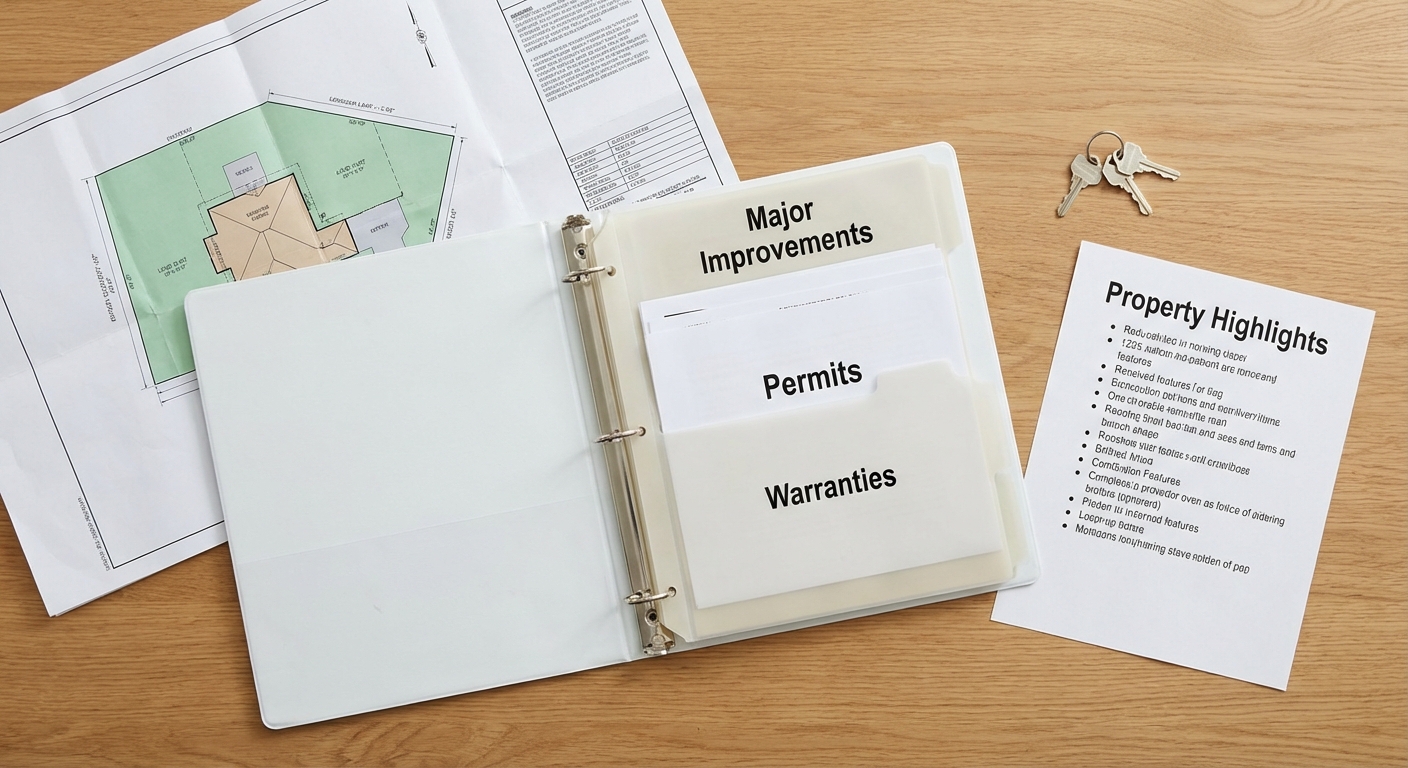

The Paper Trail: Essential Documentation for a Higher Appraisal

Providing the appraiser with well-organized documentation streamlines their process and ensures they have all the facts to justify your home’s value.

Why Documentation Matters

Appraisers work on tight deadlines and conduct independent research. However, providing them with organized, detailed information about your property’s improvements, special features, and compliance helps them make appropriate positive adjustments and avoid undervaluing unique features.

Your Documentation Packet Should Include:

Comprehensive improvement list:

- Document ALL major upgrades and renovations from the last 5-10 years

- Include: date completed, total cost, contractor names, and permit numbers (if applicable)

- Attach copies of paid invoices, warranties, and permits

- Example format: “New Roof (30-year architectural shingles) – June 2022 – $15,000 – ABC Roofing, Permit #2022-12345”

Energy efficiency and green features:

- Solar panel documentation (specify if owned vs. leased—leased panels can complicate appraisals)

- New window specifications and installation dates

- HVAC upgrades (heat pumps, high-efficiency furnaces)

- Insulation improvements

- Earth Advantage or LEED certification documents

ADU information (if applicable):

- Permit documentation proving the ADU is legal

- Square footage and finish quality details

- Rental history if used as an income property

HOA information:

- Contact information for the Homeowners Association

- Current dues amount and what they cover

- Any pending special assessments

- CC&Rs (Covenants, Conditions, and Restrictions) summary

Legal and survey documents:

- Copy of property survey showing exact lot dimensions

- Title information

- Easements or shared access agreements

- Any relevant boundary or encroachment documentation

Strategic comparable sales:

- Your agent’s list of comparable sales used to price your home

- This is especially helpful if any comps were private sales not listed on RMLS

- Include addresses, sale dates, and prices of the best comps

Presentation Matters

Organize all documentation in a clean folder or binder with labeled tabs. Consider creating a one-page “Property Highlights” summary sheet that lists your home’s best features and recent improvements at a glance.

Smart Investments: What Actually Adds Value Before an Appraisal?

Not all pre-appraisal improvements yield equal returns. Understanding which projects appraisers value most helps you invest wisely.

High-ROI Exterior Improvements

According to Remodeling Magazine’s 2023 Cost vs. Value Report:

- Garage door replacement recoups 102.9% of its cost

- Manufactured stone veneer returns 102.3%

- Fiber-cement siding replacement recovers 88.5%

Moderate-ROI Interior Improvements

- Minor kitchen remodels (not full renovations) return approximately 85.7%

- Vinyl window replacement recovers about 68.5%

- Fresh paint and minor cosmetic updates offer excellent return for minimal investment

Portland-Specific Value Additions

- Green certifications can add measurable value in Portland’s environmentally-conscious market

- Transit proximity and high walk/bike scores are quantifiable assets

- Permitted ADUs can significantly increase value when comps are available

Improvements to Avoid Right Before Appraisal

- Major DIY renovations without proper permits

- Overly personalized upgrades that don’t appeal to broad markets

- Expensive landscaping projects with limited appraisal impact

- Swimming pools in Portland’s climate (often don’t add proportional value)

Strategic Timing

If you’re planning to sell within 6-12 months, focus on high-impact, lower-cost improvements: deep cleaning, paint, minor repairs, and curb appeal enhancements. Save major renovations for after the sale unless they’re necessary to make the home marketable.

Key Takeaways

Preparing your Portland home for a successful appraisal isn’t about perfection—it’s about presenting your property professionally, addressing obvious issues that could lower your condition rating, and providing appraisers with the documentation they need to justify your home’s true market value. The difference between a C3 and C4 condition rating, or between a well-documented improvement and one the appraiser overlooks, can easily represent tens of thousands of dollars in a $575,000 median market. By following this comprehensive checklist—maximizing curb appeal, completing minor repairs, ensuring Oregon safety compliance, and assembling thorough documentation—you’re taking control of the factors within your influence. Remember: while you can’t control market conditions or which comparable sales the appraiser selects, you absolutely can control how your home is presented on appraisal day. These proactive steps don’t just increase your chances of a favorable valuation—they demonstrate to buyers and their lenders that your home has been meticulously maintained, building confidence throughout the entire transaction. Ready to list your Portland home? Start this checklist 2-3 weeks before your anticipated appraisal date. Your future self (and your bank account) will thank you.

Ready to Maximize Your Home’s Value?

For expert guidance through every step of your Portland home sale, including appraisal preparation and negotiation support, contact GW Hartley IV today.

References:

- National Association of REALTORS®. (June 2024). REALTORS® Confidence Index Survey: May 2024. Retrieved from https://www.nar.realtor/research-and-statistics/research-reports/realtors-confidence-index

- RMLS™. (June 2024). Market Action, May 2024. Retrieved from https://www.rmlsweb.com/v2/public/marketstats.asp

- The Appraisal Foundation. (n.d.). Uniform Standards of Professional Appraisal Practice (USPAP). Retrieved from https://www.appraisalfoundation.org/imis/TAF/Standards/Appraisal_Standards/Uniform_Standards_of_Professional_Appraisal_Practice/TAF/USPAP.aspx

- Fannie Mae. (June 2023). Uniform Residential Appraisal Report (Form 1004). Retrieved from https://singlefamily.fanniemae.com/media/24561/display

- American National Standards Institute (ANSI). (2021). ANSI Z765-2021: Standard For Calculating Square Footage. Fannie Mae Summary. Retrieved from https://singlefamily.fanniemae.com/media/30206/display

- Fannie Mae. (October 2023). B4-1.3-06, Property Condition and Quality of Construction of the Improvements. Selling Guide. Retrieved from https://selling-guide.fanniemae.com/Selling-Guide/Part-B-Origination-thru-Closing/Subpart-B4-Underwriting-Property/Chapter-B4-1-Property-Assessment/Section-B4-1-3-Appraisal-Report-Assessment/1032992521/B4-1-3-06-Property-Condition-and-Quality-of-Construction-of-the-Improvements.htm

- U.S. Department of Housing and Urban Development (HUD). (September 2015). Valuation Protocol, Appendix D: Valuation Protocol and Appraiser Requirements. Retrieved from https://www.hud.gov/sites/documents/40001D4SEC.PDF

- U.S. Department of Energy. (2021). Selling into the Sun: Price Premium Analysis of a Multi-State Dataset of Solar Homes. Lawrence Berkeley National Laboratory. Retrieved from https://emp.lbl.gov/publications/selling-sun-price-premium-analysis

- The Appraisal Institute. (2022). Valuing Accessory Dwelling Units. Retrieved from https://www.appraisalinstitute.org/assets/1/7/Valuation-mag-2022-Issue-3-feature-Valuing-Accessory-Dwelling-Units.pdf

- University of Alabama, Culverhouse College of Business. (April 2021). What is Curb Appeal and How Much is it Worth? Retrieved from https://cba.ua.edu/news/2021/04/what-is-curb-appeal-and-how-much-is-it-worth

- International Code Council. (2021). International Residential Code (IRC) R311.7.8 Handrails. Retrieved from https://codes.iccsafe.org/content/IRC2021P2/chapter-3-building-planning#IRC2021P2_Pt03_Ch03_SecR311.7.8

- Oregon State Legislature. (2023). ORS 479.270: Location of smoke alarms and smoke detectors. Retrieved from https://www.oregonlegislature.gov/bills_laws/ors/ors479.html

- Oregon State Legislature. (2023). ORS 476.725: Carbon monoxide alarms. Retrieved from https://oregon.public.law/statutes/ors_476.725

- Federal Emergency Management Agency (FEMA). (April 2021). How To Secure Your Water Heater. Retrieved from https://www.fema.gov/sites/default/files/documents/fema_how-to-secure-your-water-heater.pdf

- Zonda Media. (2023). 2023 Cost vs. Value Report. Remodeling Magazine. Retrieved from https://www.remodeling.hw.net/cost-vs-value/2023/