Table of Contents

- The Economic Forces Reshaping Portland Real Estate

- Inside Portland’s Housing Market: Current Conditions and Local Challenges

- Why 2026 Could Be the Best Buyer’s Market in a Decade

- Selling in 2026: Why Strategy Matters More Than Ever

- What Could Change the Game: UGB Expansion and Insurance Concerns

- Key Takeaways

Portland’s housing market is experiencing a fundamental shift from a prolonged seller’s market toward equilibrium—the most balanced conditions in over a decade. After years of rapid price appreciation and volatile mortgage rates, the market is finally stabilizing with median home values at $516,539, down 1.5% year-over-year. Mortgage rates are projected to average around 6.0% for 2026—a significant improvement from the 7-8% range, though far from the ultra-low rates of 2010-2021. This transition creates distinct opportunities and challenges for both buyers and sellers that require new strategies. The national housing market is expected to see a 14% increase in existing-home sales, signaling renewed activity. However, Portland faces unique local headwinds, including job losses of 40,000 positions from pre-pandemic peaks and a record 27.3% downtown office vacancy rate. This insider’s forecast breaks down the economic indicators, market trends, and strategic considerations that will define Portland real estate in 2026, helping you make informed decisions whether you’re buying or selling.

The Economic Forces Reshaping Portland Real Estate

Understanding the broader economic context is essential for navigating Portland’s 2026 housing market. National monetary policy and interest rate trends set the foundation for local market conditions, influencing everything from mortgage affordability to buyer confidence.

Federal Reserve Holding Steady

The Federal Reserve is likely to maintain its policy rate for most of 2026, with only modest cuts possible if economic conditions warrant. This measured approach creates a more predictable environment for buyers compared to the volatility of recent years. The Fed’s cautious stance reflects its dual mandate of managing inflation while supporting employment, and current projections suggest stability rather than dramatic shifts.

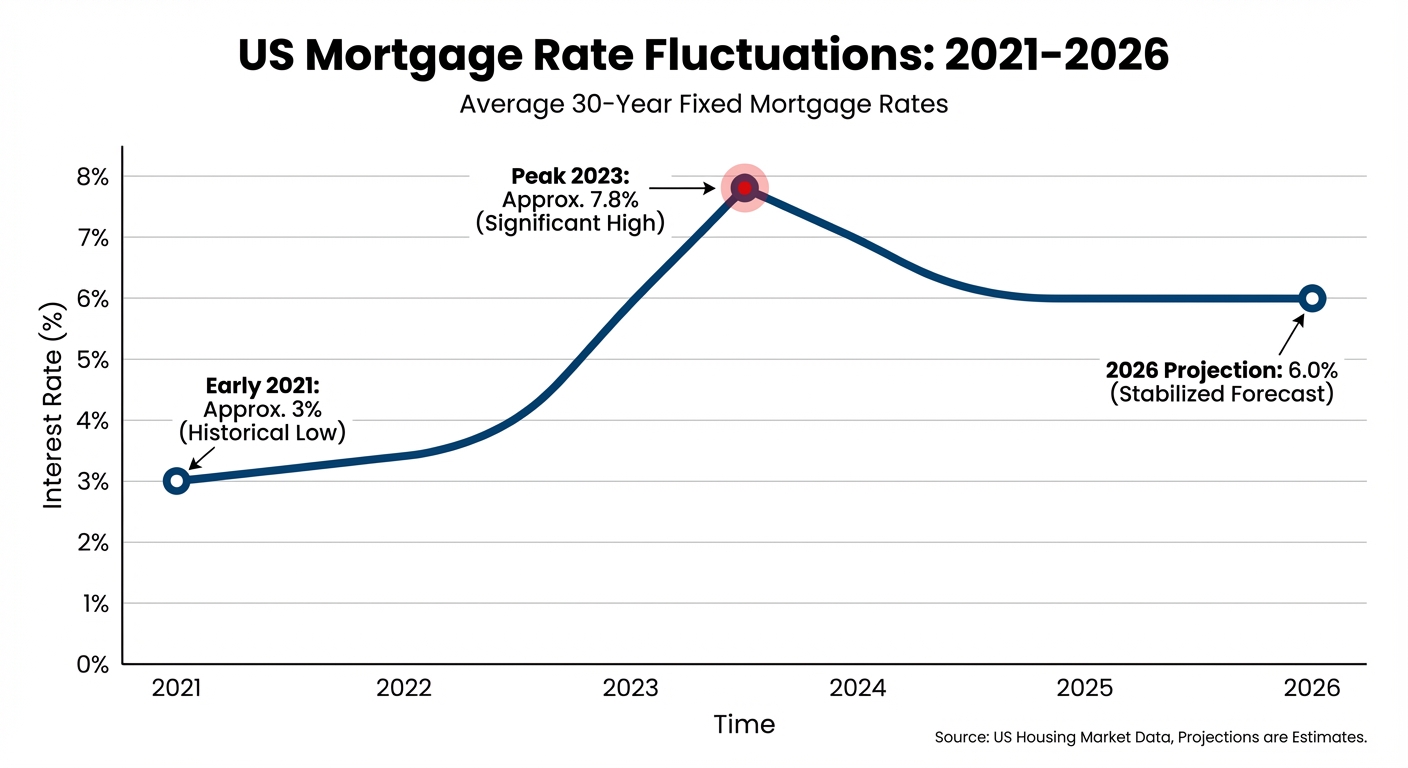

Mortgage Rate Stabilization: The New Normal

30-year fixed mortgage rates averaging 6.0% represent a “new normal” that buyers should accept rather than resist. The era of 3% rates is firmly in the rearview mirror, and waiting for a return to those levels means missing opportunities in today’s market.

The chart above illustrates the dramatic journey mortgage rates have taken from the pandemic-era lows through the 2023-2024 peaks, settling into today’s more moderate—but still elevated—range. This stabilization, while higher than historical lows, provides the predictability that both buyers and sellers need to make confident decisions.

National Market Rebound on the Horizon

The National Association of Realtors forecasts a significant 14% jump in existing-home sales for 2026, driven by stable rates and resilient employment. According to Lawrence Yun, NAR’s chief economist, “The housing market is set for a comeback as mortgage rates stabilize and more inventory becomes available to meet pent-up demand.” However, this rebound isn’t uniform across all price points. Upper-end homes ($750,000 to $1 million) are seeing the strongest sales growth, while inventory in lower price brackets remains constrained. This bifurcation creates particular challenges for first-time buyers trying to enter the market.

No Housing Crash on the Horizon

Despite concerns about market corrections, a significant price downturn remains unlikely. Homeowners with substantial equity and low existing mortgage rates aren’t forced into distressed sales. This strong equity position, combined with strict lending standards implemented after the 2008 financial crisis, creates a fundamentally different environment than the last housing crash.

Inside Portland’s Housing Market: Current Conditions and Local Challenges

While national trends provide important context, Portland’s market has unique characteristics that set it apart from other major metros. Understanding these local dynamics is crucial for making informed real estate decisions in 2026.

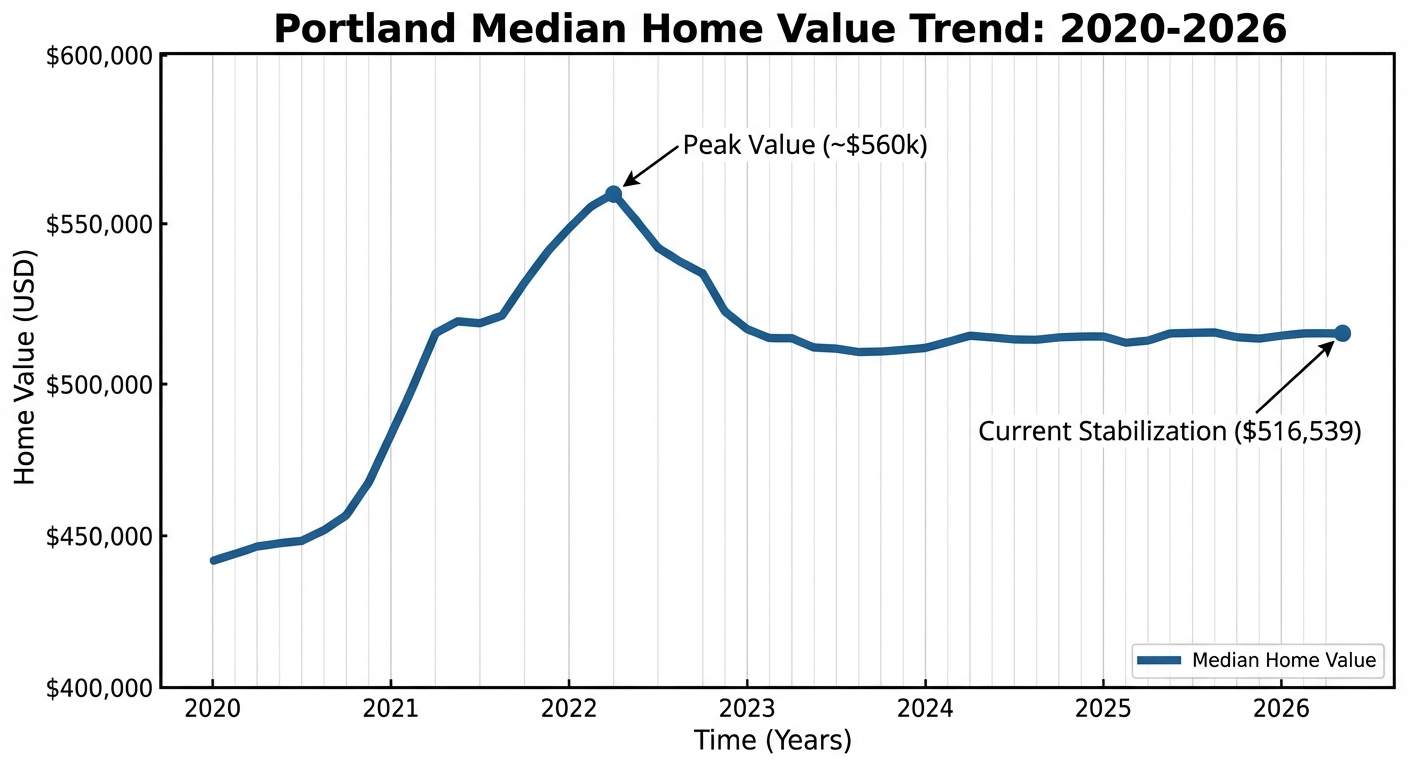

Price Stabilization After Years of Growth

Portland’s median home value of $516,539 represents a 1.5% decline year-over-year, marking a departure from the rapid appreciation of the pandemic era. However, the median sale price actually increased 3.0% to $500,000, indicating that while appraised values have softened slightly, actual transaction prices remain stable. This suggests the market is finding equilibrium rather than experiencing a collapse.

The trend line above shows Portland’s home value trajectory from the pandemic boom through today’s stabilization. Notice how the sharp appreciation has leveled off into a more sustainable, balanced pattern—healthy for long-term market stability.

Inventory Improvements Change the Game

Homes are now staying on market an average of 42 days, up from 38 days previously. While this may seem modest, it represents a meaningful shift in market dynamics. Projected supply is reaching 4.6 months of inventory—approaching the 5-6 month range that economists consider a balanced market. For context, during the height of the seller’s market, inventory often measured less than one month, creating the frenzied bidding wars that defined the 2020-2022 era. Today’s improving inventory levels mean buyers have time to conduct proper due diligence, negotiate thoughtfully, and avoid feeling pressured into hasty decisions.

Portland Metro Housing Market Indicators (Early 2026)

| Metric | Value | Year-Over-Year Change |

|---|---|---|

| Median Home Value | $516,539 | -1.5% |

| Median Sale Price | $500,000 | +3.0% |

| Median Days on Market | 42 Days | +10.5% |

The End of Bidding Wars

More balanced supply-demand dynamics mean buyers no longer face the frenzied competition of previous years. Multiple offer situations, while still possible on exceptionally priced properties, are no longer the default scenario. This shift fundamentally changes the buyer’s experience and negotiating position.

Portland’s Economic Headwinds

Despite positive national trends, Portland faces significant local challenges that temper enthusiasm about rapid market recovery. Multnomah County has lost approximately 40,000 jobs from its pre-pandemic peak. This isn’t merely a function of population loss but represents genuine employment decline within the region. These job losses impact housing demand, particularly among would-be first-time buyers who need stable employment to qualify for mortgages. The commercial real estate crisis compounds these challenges. Downtown office vacancy reached a record 27.3%, causing dramatic property devaluation. This devaluation directly impacts the city’s property tax revenue, which funds essential public services including schools. The cascading effects of commercial real estate struggles extend beyond office workers to the entire urban ecosystem. Perhaps most telling, the Emerging Trends in Real Estate® 2026 report ranked Portland 80th out of 81 U.S. markets for investment and development prospects. This rock-bottom ranking reflects institutional investors’ lack of confidence in Portland’s near-term outlook, which can become a self-fulfilling prophecy as capital flows to more favored markets.

Why 2026 Could Be the Best Buyer’s Market in a Decade

For buyers who have been waiting on the sidelines, 2026 presents a rare window of opportunity. The combination of improved inventory, stabilized mortgage rates, and sellers’ willingness to negotiate creates conditions not seen since before the pandemic.

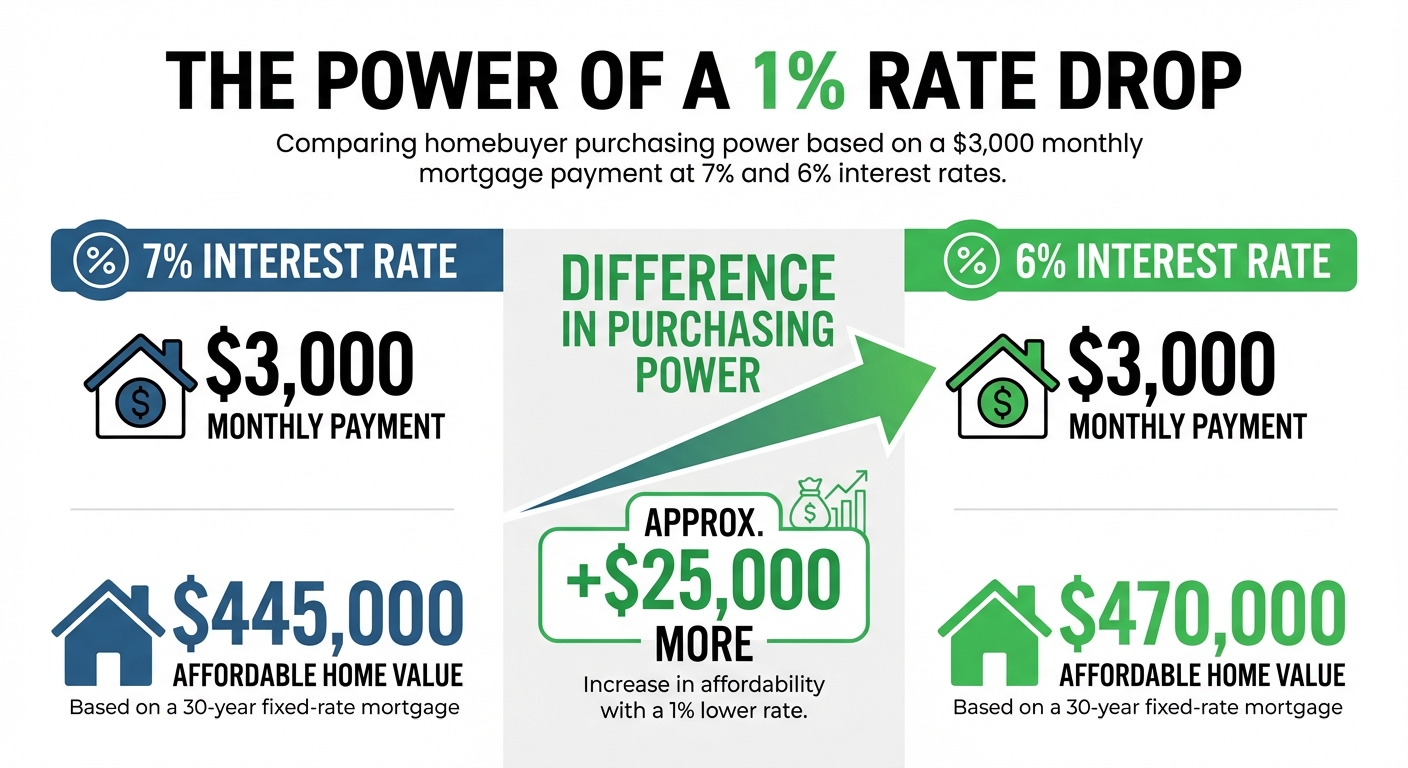

Improved Affordability & Purchasing Power

The impact of mortgage rate changes on purchasing power is substantial and often underestimated. A one-percentage-point drop in mortgage rates allows buyers with a $3,000 monthly budget to afford approximately $25,000 more in home value.

This infographic illustrates the real-world impact of rate changes on your monthly budget and total purchasing power. For many buyers, the difference between 7% and 6% rates means the difference between stretching for a starter home and affording something that truly meets their needs. Consider this example: A $500,000 home at 7% interest costs approximately $3,326 per month (principal and interest only). That same home at 6% costs $2,998 per month—a savings of $328 monthly or nearly $4,000 annually. Over a 30-year mortgage, this represents over $100,000 in interest savings.

Negotiating Leverage Returns

Buyers can now negotiate on price, request repairs, and include contingencies that were “unthinkable” during market peaks. Inspection contingencies, appraisal contingencies, and financing contingencies—protections that buyers routinely waived during bidding wars—are once again standard parts of purchase agreements. Multiple offer scenarios have decreased significantly, giving buyers time to conduct thorough due diligence. You can schedule home inspections, review neighborhood data, and consult with contractors about potential renovation costs without fear that another buyer will swoop in with a superior offer. Sellers are more willing to cover closing costs or make concessions to secure qualified buyers. In a balanced market, a bird in hand (a qualified buyer with reasonable requests) is worth far more than the hypothetical better offer that might never materialize.

First-Time Buyer Considerations

Despite these improvements, first-time buyers still face significant challenges. Nationally, the first-time buyer share has fallen to historic lows due to affordability pressures. High student loan debt, stagnant wage growth relative to home prices, and the challenge of saving for down payments while paying rent create formidable barriers. However, Portland offers valuable resources for those willing to explore their options. The City of Portland’s Down Payment Assistance Loan (DPAL) program offers favorable, forgivable loans that can make the difference between renting indefinitely and achieving homeownership. The DPAL program provides qualified buyers with loans for down payments and closing costs. These loans feature below-market interest rates and, critically, include forgiveness provisions for buyers who remain in their homes for specified periods. Additional programs like the Oregon Bond Residential Loan Program offer competitive rates for qualified first-time buyers.

Strategic Actions for Buyers

Actionable Tips for 2026 Buyers

- Get fully pre-approved (not just pre-qualified) before starting your search. Pre-qualification involves a soft review of your finances; pre-approval requires full documentation and underwriter review. Sellers and their agents take pre-approved buyers far more seriously.

- Explore different neighborhoods, as market conditions vary significantly across the Portland metro area. While downtown and close-in eastside neighborhoods face headwinds, suburban communities and emerging areas may offer better value.

- Factor in rising insurance costs, especially for properties near forested areas with wildfire risk. A home that seems affordable based on mortgage payments alone may become financially stressful when you add $3,000-5,000 annually for property insurance in high-risk zones.

Selling in 2026: Why Strategy Matters More Than Ever

For sellers, 2026 requires a fundamental shift in mindset and strategy. The days of listing a property at an aspirational price and receiving multiple offers within 48 hours are over. Success now requires preparation, realistic pricing, and strategic positioning.

The Pricing Imperative

Overpricing is the biggest mistake sellers make in a balanced market. When buyers have options, they simply move on to better-priced alternatives rather than negotiating on overpriced properties. Homes priced accurately from the start sell faster and often for more than those that start too high and stagnate on the market. Data-driven pricing using recent comparable sales—not aspirational pricing based on peak market values—is essential. Your home may have been worth $550,000 in 2022, but if comparable homes are selling for $515,000 today, pricing at $545,000 “to leave room for negotiation” simply means your home sits unsold while buyers purchase competing properties.

Presentation & Condition

With more inventory available, buyers favor move-in-ready homes. Deferred maintenance that sellers might have gotten away with during the frenzy now becomes a deal-killer or negotiating point. Strategic pre-listing investments pay dividends. Necessary repairs, fresh interior paint in neutral colors, professional staging, and curb appeal improvements help your home stand out. These investments typically return multiples of their cost by reducing days on market and preserving your negotiating position. Professional photography and virtual tours are now standard expectations, not luxuries. In an era where 90% of buyers begin their search online, poor photos doom your listing before buyers ever schedule a showing. Investing $300-500 in professional photography is one of the highest-return investments you can make.

The “Lock-In Effect” Thaws

Many homeowners with ultra-low mortgage rates (the “lock-in effect”) are beginning to re-enter the market as life events necessitate moves. Job relocations, growing families, aging parents, and other life changes eventually override the financial benefit of a low mortgage rate. As rates have stabilized, the psychological barrier of accepting a higher-rate mortgage has lessened. A homeowner with a 3% mortgage evaluating whether to move faces a significant financial impact by taking on a 6% rate. However, as rates stabilize rather than continuing to rise, that homeowner can plan with more confidence, knowing they’re not jumping into a volatile environment.

Market Time Expectations

Average 42 days on market means sellers should plan for 45-60 days from listing to closing, assuming no complications. Quick sales still happen for exceptionally priced, well-presented properties in desirable locations, but these are outliers rather than the norm. Homes that linger beyond 60 days typically require price adjustments to generate renewed buyer interest. The longer a property sits, the more buyers wonder what’s wrong with it, creating a downward spiral in perceived value.

Strategic Actions for Sellers

Actionable Tips for 2026 Sellers

- Work with an experienced agent to determine a competitive, data-driven list price based on recent sales of truly comparable properties. Your agent’s opinion of value should be supported by specific comparable sales data, not merely gut feeling.

- Be flexible and responsive during negotiations. In balanced markets, first offers are often best offers. While you shouldn’t accept lowball offers, reasonable offers from qualified buyers deserve serious consideration.

- Consider timing carefully. Spring market (March-June) typically sees highest buyer activity, though less competition from other sellers during off-peak periods can sometimes offset lower buyer activity.

- Disclose known issues upfront to avoid deal-killing surprises during inspection. Buyers understand that homes aren’t perfect, but they despise feeling deceived.

What Could Change the Game: UGB Expansion and Insurance Concerns

Beyond standard market indicators, several Portland-specific factors could significantly influence real estate dynamics in ways that national trends don’t capture.

Urban Growth Boundary (UGB) Expansion

Metro is considering expanding the UGB in 2026, potentially adding thousands of acres of buildable land in suburban areas like Hillsboro and Wilsonville. This decision carries implications that extend well beyond the immediate areas affected. The timeline reality is important to understand: first homes from expansion wouldn’t be delivered until 2027-2029, but the decision itself could influence land speculation and long-term price expectations in outer suburbs. Developers begin acquiring land and planning projects years before homes reach market, and their activity signals future supply increases. This potential expansion could impact urban vs. suburban price dynamics. If significant new suburban inventory is coming online in 2-3 years, buyers with flexibility may choose to wait, putting downward pressure on current suburban prices. Conversely, urban properties close to employment centers might hold value better if the expansion primarily affects distant suburbs with longer commutes. For buyers willing to look at emerging areas with longer-term appreciation potential, understanding the UGB expansion timeline and likely affected areas provides strategic advantage. Early movers to areas designated for expansion but not yet developed can benefit from appreciation as infrastructure and services follow residential development.

Insurance and Environmental Risks

Rising concern about the increasing cost and decreasing availability of homeowner’s insurance represents a significant challenge, particularly due to wildfire risk. Several major insurers have reduced their Oregon exposure or stopped writing new policies in high-risk areas. Pending legislation would require insurers to account for wildfire mitigation efforts made by homeowners, potentially alleviating cost pressures. If homeowners who implement Firewise USA® mitigation measures—creating defensible space, using fire-resistant materials, managing vegetation—receive insurance discounts or improved availability, this could influence both property values and buyer demand in affected areas.

Insurance Questions to Ask Before Buying

- Is insurance available through standard carriers, or only through high-cost specialty insurers?

- What’s the annual premium, and how does it compare to similar homes in lower-risk areas?

- Has the property implemented Firewise USA® mitigation measures that might reduce insurance costs?

Insurance considerations that seemed peripheral just a few years ago now rank alongside location, condition, and price as fundamental factors in purchase decisions. Properties in high-risk areas without mitigation measures may become increasingly difficult to sell or finance as lenders require proof of insurance as a condition of lending.

Neighborhood-Level Variations

Market conditions vary significantly across Portland metro neighborhoods. While downtown and inner eastside neighborhoods face challenges related to commercial vacancies and urban livability concerns, suburban communities like Lake Oswego, West Linn, and Tigard show more stability. Emerging neighborhoods in outer East Portland and Clackamas County offer opportunities for buyers willing to accept longer commutes in exchange for more affordable entry points and potential appreciation. Research specific neighborhood trends before making assumptions based on metro-wide data—the “Portland market” is really dozens of distinct micro-markets with their own supply-demand dynamics.

Key Takeaways

Portland’s 2026 market represents a historic shift toward balance after years of extreme seller advantages. This normalization, while potentially disappointing for sellers who hoped to replicate peak-market sales prices, creates a healthier, more sustainable market environment. For buyers, this is the most favorable environment in over a decade, with improved inventory, stabilized rates, and negotiating power. However, affordability challenges remain, particularly for first-time buyers. Those who can overcome down payment hurdles find a market that rewards patience and thorough research rather than requiring rushed decisions and waived contingencies. For sellers, success requires strategic pricing, professional presentation, and realistic expectations. The days of multiple offers on any listed property are over. However, well-priced, properly presented homes in desirable locations still sell efficiently. The key is understanding that you’re no longer competing against historic scarcity but against other sellers in a more balanced market. Economic context matters deeply. National trends point to recovery, with increased sales activity and stable prices. However, Portland faces unique local headwinds—job losses, commercial real estate challenges, and investor confidence issues—that require careful navigation. Blanket national optimism doesn’t necessarily translate to Portland’s specific circumstances. The market isn’t crashing, but it is normalizing—a healthy development for long-term sustainability. Markets that appreciate rapidly tend to correct sharply; markets that grow steadily tend to maintain value better through economic cycles. Portland’s current stabilization, while less exciting than the pandemic boom, provides a more solid foundation for sustainable homeownership. Both buyers and sellers benefit from working with experienced local professionals who understand neighborhood-level dynamics rather than just metro-wide trends. The difference between a skilled agent who knows the nuances of specific neighborhoods and one who relies on general market knowledge can mean tens of thousands of dollars in a transaction. The “wait and see” approach carries risks on both sides. Buyers who wait may face renewed competition if inventory tightens or rates rise unexpectedly. Sellers who wait may see further price softening if economic headwinds persist or inventory continues to build. There’s no perfect moment—only informed decisions based on personal circumstances and current market realities.

Ready to Navigate Portland’s 2026 Market with Confidence?

Whether you’re buying your first home, selling after years of equity growth, or making a strategic move within the market, having the right strategy and local expertise makes all the difference.

References:

- J.P. Morgan. (2026). What’s The Fed’s Next Move? https://www.jpmorgan.com/insights/global-research/economy/fed-rate-cuts

- Sold by Salgado. (2026). Portland Real Estate Market Outlook 2026. https://soldbysalgado.com/blog-posts/2025-2026-portland-oregon-market-news-and-insights

- Hatch Homes Group. (2026). What the 2026 Housing Market Could Bring for Portland. https://hatchhomes.com/what-the-2026-housing-market-could-bring-for-portland/

- Sammamish Mortgage. (2026). Portland, OR Housing Forecast for 2026. https://www.sammamishmortgage.com/portland-or-housing-forecast/

- Redfin. (2025). Redfin’s 2026 Predictions: Welcome to The Great Housing Reset. https://www.redfin.com/news/housing-market-predictions-2026/

- National Association of REALTORS®. (2025). NAR Forecast: Home Sales Expected to Jump 14% in 2026. https://www.nar.realtor/newsroom/nar-forecast-home-sales-expected-to-jump-14-in-2026

- National Association of REALTORS®. (2025). Housing Market Set for a 2026 Comeback, NAR Predicts. https://www.nar.realtor/magazine/real-estate-news/economy/housing-market-set-for-a-2026-comeback-nar-predicts

- Zillow. (2026). Portland, OR Housing Market. https://www.zillow.com/home-values/13373/portland-or/

- Redfin. (2026). Portland Housing Market: House Prices & Trends. https://www.redfin.com/city/30772/OR/Portland/housing-market

- Realtor.com. (2025). 2026 Housing Forecast. https://www.realtor.com/research/2026-national-housing-forecast/

- City of Portland. (2025). FY 2026-27 December General Fund Forecast. https://www.portland.gov/budget/2026-2027-budget/documents/fy-2026-27-general-fund-forecast/download

- Portland Business Journal. (2026). Portland office vacancy rate climbs to new high in 4th quarter. https://www.bizjournals.com/portland/news/2026/01/12/portland-office-quarterly-report-cbre.html

- Oregon Office of Economic Analysis. (2025). Oregon Economic and Revenue Forecast. https://www.oregon.gov/das/oea/Documents/OEA-Forecast-1225.pdf

- Rental Housing Alliance Oregon. (2025). Portland’s Rock-Bottom Ranking in the 2026 Emerging Trends Report. https://www.paroa.org/post/portland-s-rock-bottom-ranking-in-the-2026-emerging-trends-report-a-five-alarm-wake-up-call-for-ore

- Own It Northwest. (2026). The housing market is turning a corner in Portland, OR going into 2026. https://www.ownitnorthwest.com/blog/the-housing-market-is-turning-a-corner-in-portland-or-going-into-2026

- Portland Housing Bureau. (2026). Down Payment Assistance Loan Program. https://www.portland.gov/phb/down-payment-assistance-loan

- Metro. (2026). Urban growth boundary. https://www.oregonmetro.gov/what-metro-does/land-use-and-development/2040-growth-concept/urban-growth-boundary

- Lisa Mehlhoff Homes. (2026). Is the Urban Growth Boundary expanding in 2026? https://lisamehlhoffhomes-portlandrealtor.com/blog/Is-the-Urban-Growth-Boundary-expanding-in-2026–and-will-that-open-up-any-new-affordable-inventory-in-areas-like-Hillsboro-or-Wilsonville-

- KATU News. (2026). Oregon lawmakers look to wildfire mitigation as a path to lower home insurance costs. https://katu.com/news/local/oregon-lawmakers-look-to-wildfire-mitigation-as-a-path-to-lower-home-insurance-costs

- Portland Tribune. (2026). Oregon bill would require home insurers to consider wildfire prevention efforts. https://portlandtribune.com/2026/01/19/oregon-bill-would-require-home-insurers-to-consider-wildfire-prevention-efforts/

- Portland Monthly. (2025). Portland’s Neighborhoods by the Numbers | Real Estate Market 2025. https://www.pdxmonthly.com/home-and-real-estate/portland-real-estate-market-data-report-neighborhoods