Table of Contents

- Why Portland? Understanding the Market Fundamentals Driving Long-Term Value

- Four Proven Entry Strategies: From House Hacking to Value-Add Investing

- From Financial Prep to Deal Analysis: The Proven Process for Your First Investment

- Know Before You Invest: Portland’s Tenant-Friendly Laws and What They Mean for You

- Ready to Begin? Your Actionable Next Steps for Portland Real Estate Success

Portland, Oregon isn’t just known for its coffee culture, craft breweries, and stunning natural beauty—it’s also one of the West Coast’s most compelling real estate investment markets. Over the past decade, the Portland metropolitan area has delivered extraordinary returns for investors, with home values appreciating over 130% while maintaining a robust rental market fueled by consistent population growth and economic strength. But here’s the reality: Portland’s investment landscape is complex. The same progressive policies that make it a desirable place to live—statewide rent control, strict tenant protections, and innovative urban planning—create regulatory hurdles that can trip up unprepared investors. The median home price now sits at $535,000, which can seem daunting for first-time buyers. Yet strategic approaches like house hacking with FHA financing or developing Accessory Dwelling Units (ADUs) can make entry far more accessible than many beginners realize. This guide provides a structured, evidence-based roadmap for making your first Portland real estate investment. You’ll learn how to analyze the market fundamentals that drive long-term value, identify beginner-friendly investment strategies that actually work in this unique environment, navigate the step-by-step investment process with confidence, and understand the critical regulatory considerations that separate successful Portland investors from those who struggle. Whether you’re drawn to the wealth-building potential of multifamily properties, intrigued by Portland’s ADU-friendly policies, or simply looking to build equity through smart real estate decisions, this comprehensive guide will equip you with the knowledge you need to take that crucial first step.

Why Portland? Understanding the Market Fundamentals Driving Long-Term Value

Before committing capital to any market, savvy investors ask: What economic and demographic forces will drive property values and rental demand over the next 5, 10, or 20 years? Portland’s answer to that question is compelling.

Economic Strength and Employment Trends

Portland’s economy is refreshingly diverse. While the “Silicon Forest”—the region’s nickname for its thriving tech sector—gets significant attention, the area’s economic foundation includes healthcare, advanced manufacturing, and global brands like Nike and Adidas North America. This diversification provides resilience against industry-specific downturns. The numbers back this up. As of October 2024, the Portland-Vancouver-Hillsboro Metropolitan Statistical Area maintained an unemployment rate of just 3.9%, indicating a healthy job market that attracts and retains workers—the very people who need places to live. When employment is strong, housing demand follows.

Population Growth Fueling Housing Demand

The Portland MSA reached a population of 2,507,649 residents in July 2023, reflecting consistent growth over the past decade. This isn’t a boom-and-bust story; it’s steady, sustainable population expansion driven by the region’s quality of life, economic opportunities, and natural amenities. For investors, population growth translates directly into sustained demand for housing. More residents mean more renters, more homebuyers, and upward pressure on both rents and property values.

Housing Market Dynamics

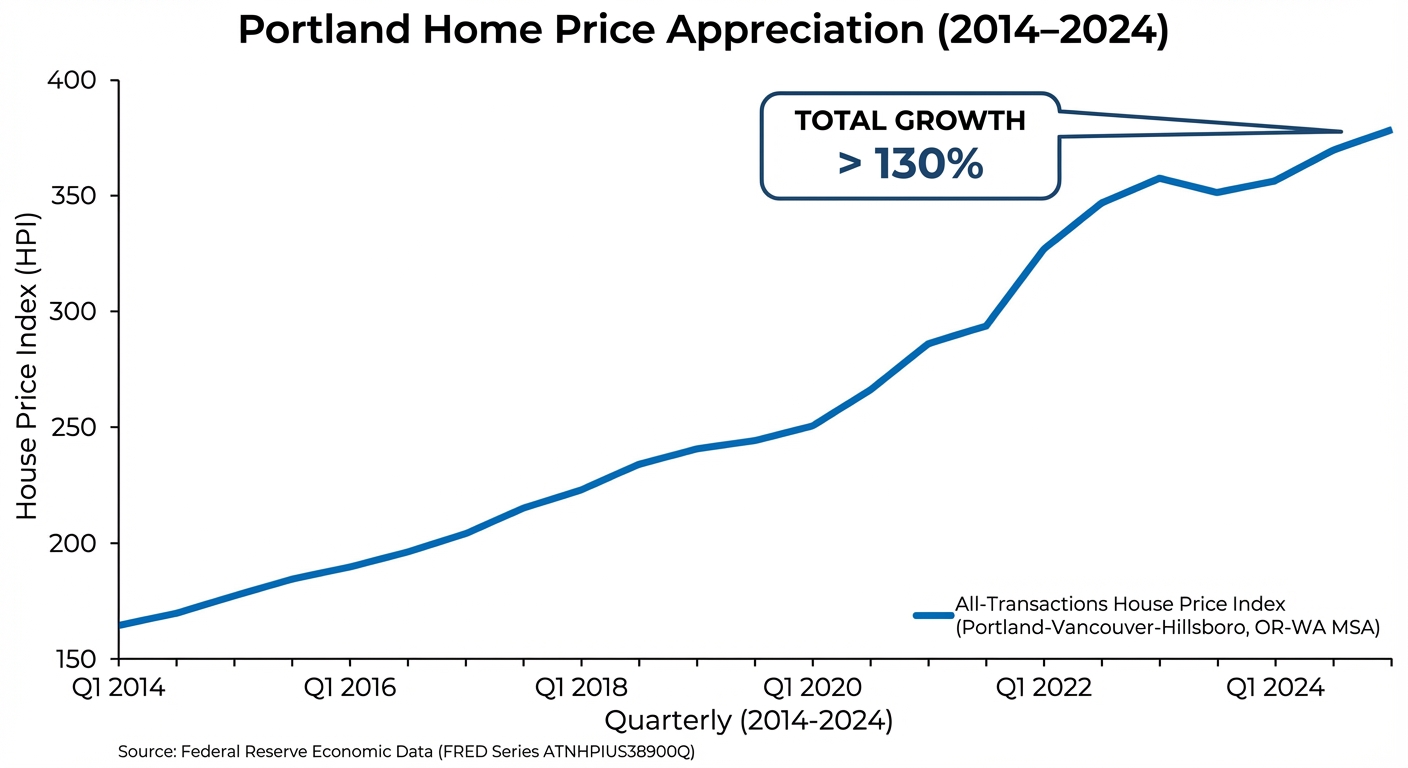

Portland’s housing market tells a story of constrained supply meeting persistent demand: Median Home Prices: The current median sale price of $535,000 reflects decades of strong appreciation. According to Federal Reserve data, Portland-area home values have surged over 130% from 2014 to 2024—a compound annual growth rate that significantly outpaces inflation and provides compelling evidence of the market’s long-term wealth-building potential.

Market Inventory: As of October 2024, Portland had just 3.2 months of housing inventory. Real estate professionals consider 4-6 months a “balanced” market; anything below 4 months favors sellers. This tight inventory environment creates competition for available properties and supports price stability even during economic uncertainty.

The Rental Market Opportunity

For investors focused on rental income, Portland’s fundamentals are equally encouraging: Low Vacancy Rates: A 4.4% vacancy rate in the fall of 2023 signals a healthy, competitive rental market. When vacancy rates are low, landlords have negotiating power, and rental income remains stable. Attractive Rent Levels: Average rents of $1,535 for one-bedroom units and $1,757 for two-bedroom apartments provide solid baseline projections for rental income analysis. These figures reflect the reality that Portland renters are willing to pay premium rents to live in desirable neighborhoods with access to urban amenities.

The Urban Growth Boundary: Portland’s Secret Weapon

Perhaps no single policy has shaped Portland’s real estate market more profoundly than the Urban Growth Boundary (UGB). Established in 1979 by Metro, the regional government, the UGB is a legal line drawn around the metropolitan area. Development is largely prohibited outside this boundary, protecting surrounding farms and forests from urban sprawl. How It Works: Rather than allowing cities to sprawl indefinitely into rural areas—as happens in many American metros—the UGB forces development inward. Cities must grow “up” rather than “out,” encouraging higher-density housing like townhomes, condos, and the duplexes and triplexes that are goldmines for house-hacking investors. Why It Matters for Investors: The UGB creates long-term land scarcity. With a finite supply of developable land inside the boundary and a consistently growing population, basic economics dictate upward pressure on property values. This isn’t speculation—it’s the fundamental supply-and-demand dynamic that has driven Portland’s 130% appreciation over the past decade. The UGB is effectively a moat around your investment, a structural force that supports long-term value regardless of short-term market fluctuations.

Portland Metro Area Key Real Estate Metrics (2023-2024)

| Metric | Value/Rate | Context |

|---|---|---|

| MSA Population (July 2023) | 2,507,649 | Steady long-term growth |

| Median Home Sale Price (Oct 2024) | $535,000 | Reflects high demand and appreciation |

| 10-Year Home Price Index Growth | +130% | Demonstrates strong long-term appreciation |

| Housing Inventory (Oct 2024) | 3.2 Months | Indicates a competitive seller’s market |

| Rental Vacancy Rate (Fall 2023) | 4.4% | Signifies strong and stable tenant demand |

Four Proven Entry Strategies: From House Hacking to Value-Add Investing

Now that you understand why Portland’s fundamentals are compelling, let’s explore how beginners can actually enter this market. Not all investment strategies are created equal—some require significantly more capital, expertise, or risk tolerance than others. Here are four proven approaches, ranked from most accessible to most advanced.

Strategy 1: House Hacking with Small Multifamily (2-4 Units)

House hacking is the single best strategy for beginners with limited capital. The concept is elegantly simple: purchase a duplex, triplex, or fourplex; live in one unit; and rent out the others. The rental income from your tenants offsets—or in ideal cases, completely covers—your mortgage payment, allowing you to live essentially for free while building equity. The Financing Advantage: This is where house hacking becomes genuinely accessible. The Federal Housing Administration offers loans for owner-occupied properties of up to four units with down payments as low as 3.5%. Compare that to the 20-25% down typically required for investment properties, and you see why house hacking is the entry point for so many successful investors. On a $500,000 property, 3.5% down is just $17,500—plus closing costs, you’re looking at roughly $25,000 total to get started. That’s far more achievable than the $100,000+ required for a traditional investment property purchase. Portland’s Perfect Inventory: Portland’s historic neighborhoods—particularly in Southeast and Northeast—are filled with the exact types of properties that work for house hacking. These areas developed in the early-to-mid 20th century when duplexes and triplexes were common building types. Today, these well-located properties offer both investment potential and quality of life.

Investor Insight: Beyond the financial benefits, house hacking provides an invaluable education in property management. You’ll learn tenant screening, lease agreements, maintenance coordination, and communication—all while living on-site to handle issues quickly. By the time you’re ready for your second investment property, you’ll have a year or more of hands-on experience under your belt.

Strategy 2: The ADU (Accessory Dwelling Unit) Strategy

Portland has emerged as a national leader in promoting ADU development. An ADU is a secondary, independent housing unit on a single-family residential lot—think of a small cottage in the backyard, a converted garage, or a basement apartment with its own entrance and full kitchen. Portland’s Regulatory Environment: The City of Portland has gone further than almost any other major city to encourage ADU construction. The Bureau of Development Services has streamlined permitting processes, and the city has waived System Development Charges for ADUs under certain size thresholds. These are significant savings—SDCs can run into the tens of thousands of dollars for new construction. The ROI Case: An ADU creates a new income stream from a property you may already own. If you purchase a single-family home with ADU potential, you’re essentially creating a duplex without paying duplex prices. Average rents of $1,500-$1,800 for Portland ADUs provide strong ongoing returns. But there’s another angle: property value enhancement. Research from Attom Data Solutions found that properties with ADUs command up to a 35% sale-price premium compared to similar homes without them. Whether you hold the property long-term for rental income or sell it after development, an ADU adds substantial value. Construction Considerations: ADU construction typically costs $150,000-$300,000 depending on size and finish level. While not cheap, this investment can often be financed through home equity lines of credit (HELOCs), construction loans, or cash-out refinances on properties with sufficient equity.

Strategy 3: Traditional Long-Term Rental (Buy and Hold)

The classic buy-and-hold strategy involves purchasing a property—whether a single-family home, condo, or small multifamily—and holding it for an extended period. You generate income from rent while the property appreciates, building wealth through both cash flow and equity growth. Success Factors: This strategy sounds simple, but success requires careful execution:

- Property Selection: Choose neighborhoods with strong tenant demand, low vacancy rates, and a history of stable appreciation. Neighborhoods near major employers, good schools, and public transit typically outperform.

- Financial Analysis: Accurate projections for rental income, operating expenses, and debt service are critical. Overestimating rents or underestimating expenses leads to negative surprises.

- Tenant Quality: Thorough screening processes (while adhering to Fair Housing laws) help you find reliable tenants who pay on time and maintain your property.

⚠️ Key Consideration: Buy-and-hold investing provides two distinct return streams. First, monthly cash flow—the difference between rental income and all expenses. Second, long-term appreciation—Portland’s 130% growth over the past decade demonstrates this powerfully. Many investors accept breakeven or slightly negative cash flow in high-appreciation markets because the equity gains far exceed any short-term losses.

Strategy 4: BRRRR Method (Advanced)

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—is an advanced strategy that allows experienced investors to scale their portfolios rapidly. Here’s how it works:

- Buy: Purchase a distressed property below market value (often through direct-to-seller marketing or off-market deals).

- Rehab: Renovate the property to increase both its value and rental appeal. This often means significant construction work.

- Rent: Place a quality tenant in the property, establishing a cash flow stream and demonstrating its value to lenders.

- Refinance: After the property has appreciated due to your improvements (and you’ve held it for at least 6-12 months), perform a cash-out refinance based on the new, higher appraised value.

- Repeat: Use the cash pulled out from the refinance as a down payment for your next investment property.

Why It’s Powerful: BRRRR allows you to recycle your initial capital. If you buy right and execute the renovation successfully, you can pull out most or all of your invested capital through the refinance, leaving you with a cash-flowing rental property with little to none of your own money still in the deal. Why It’s Advanced: This strategy requires substantial capital (for both purchase and renovation), knowledge of construction and project management, relationships with contractors, and higher risk tolerance. It’s not recommended for first-time investors, but it’s worth understanding for your long-term investment education.

Comparison of Beginner Investment Strategies

| Strategy | Initial Capital | Management Intensity | Risk Level | Scalability |

|---|---|---|---|---|

| House Hacking | Low (w/ FHA) | High (self-manage) | Low-Medium | Slow |

| ADU Strategy | Medium-High (construction costs) | Medium | Low-Medium | Slow (one per property) |

| Traditional Rental | High (20-25% down) | Low (w/ manager) | Medium | Medium |

| BRRRR Method | High (purchase + rehab) | Very High | High | High |

From Financial Prep to Deal Analysis: The Proven Process for Your First Investment

Understanding strategies is one thing; executing them requires a systematic approach. Here’s the proven process that successful Portland investors follow, broken down into actionable steps.

Step 1: Financial Preparation

Before you start looking at properties, you need to know exactly what you can afford and demonstrate to sellers that you’re a serious, qualified buyer. Down Payment Requirements: Your down payment needs depend entirely on your strategy:

- House Hacking (Owner-Occupied Multifamily): FHA loans allow as little as 3.5% down on properties up to 4 units, provided you live in one of them.

- Traditional Investment Property: Conventional loans typically require 20-25% down for non-owner-occupied properties.

Mortgage Pre-Approval: Getting pre-approved by a lender is non-negotiable. This process involves:

- Verifying your income through pay stubs, tax returns, and W-2s

- Checking your credit score and history

- Calculating your debt-to-income ratio

- Providing documentation of assets (bank statements, investment accounts)

A pre-approval letter shows sellers you’re financially capable and serious about purchasing. In Portland’s competitive market, offers without pre-approval are often ignored. Financial Health Factors:

- Credit Score: Most investment property loans require scores of at least 620, with better rates available for scores above 720.

- Debt-to-Income Ratio: Lenders typically want your total monthly debt payments (including the new mortgage) to be less than 43-45% of your gross monthly income.

- Cash Reserves: Lenders often want to see 3-6 months of mortgage payments, property taxes, and insurance in liquid reserves after closing.

Step 2: Building Your Expert Team

No investor succeeds in isolation. The quality of your professional team often determines the quality of your investments. Investment-Focused Real Estate Agent: Not all agents understand investment properties. You need an agent who:

- Analyzes properties based on numbers, not just aesthetics

- Has experience with multifamily properties and rental markets

- Understands cap rates, cash-on-cash returns, and market rent comparisons

- Can identify off-market opportunities or pocket listings

Mortgage Broker: A broker who specializes in investment property loans can:

- Compare offerings from multiple lenders

- Navigate more complex loan products (especially for multifamily properties)

- Advise on creative financing structures

- Help you understand the differences between conventional, FHA, and portfolio loans

Property Inspector: This is one area where you absolutely cannot cut corners. A thorough inspector will:

- Identify structural issues, roof condition, foundation problems

- Evaluate mechanical systems (HVAC, plumbing, electrical)

- Estimate remaining useful life for major components

- Flag code violations or safety hazards

A good inspection can save you tens of thousands of dollars by either negotiating repairs with the seller or walking away from a money pit. Property Manager: If you don’t plan to self-manage, interview property management companies early. Look for:

- Experience managing your type of property in your target neighborhoods

- Transparent fee structures (typically 8-10% of gross rents plus leasing fees)

- Strong tenant screening processes that comply with Portland’s FAIR ordinance

- Clear communication and technology systems for financial reporting

Step 3: Analyzing Potential Deals

This is where many beginners get overwhelmed. Real estate analysis involves multiple metrics, and it’s critical to understand what each one tells you about a property’s performance. Net Operating Income (NOI): This is your starting point for any rental property analysis.

Formula: NOI = Gross Rental Income – Operating Expenses

Operating expenses include:

- Property taxes

- Insurance

- Maintenance and repairs

- Property management fees (if applicable)

- Utilities paid by the owner

- HOA fees

- Capital expenditures reserve

Important: NOI excludes your mortgage payment. That comes later. Capitalization (Cap) Rate: The cap rate helps you compare different properties and understand their yield.

Formula: Cap Rate = NOI ÷ Purchase Price

A cap rate of 4-6% is common in appreciating markets like Portland, while higher cap rates (7-10%+) are typically found in more cash-flow-oriented, slower-appreciation markets. Cash-on-Cash Return: This is arguably the most important metric for beginners because it measures the return on your actual invested capital.

Formula: Cash-on-Cash Return = Annual Pre-Tax Cash Flow ÷ Total Cash Invested

Your “total cash invested” includes your down payment, closing costs, and any immediate repairs or improvements needed.

Sample Deal Analysis: Portland Duplex Example

Let’s walk through a real example using current Portland market conditions:

| Financial Metric | Calculation | Value |

|---|---|---|

| Purchase Price | — | $700,000 |

| Down Payment (20%) | $700,000 × 0.20 | $140,000 |

| Total Cash Invested | Down Payment + Closing Costs (~2%) | $154,000 |

| Gross Monthly Rent | Unit 1: $1,900; Unit 2: $1,900 | $3,800 |

| Gross Annual Rent | $3,800 × 12 | $45,600 |

| Annual Operating Expenses | Taxes, Insurance, Maint. (~35%) | -$15,960 |

| Net Operating Income (NOI) | $45,600 – $15,960 | $29,640 |

| Cap Rate | $29,640 ÷ $700,000 | 4.23% |

| Annual Mortgage Payment | Principal & Interest on $560k loan @ 7% | -$44,704 |

| Annual Pre-Tax Cash Flow | $29,640 – $44,704 | -$15,064 |

| Cash-on-Cash Return | -$15,064 ÷ $154,000 | -9.78% |

Step 4: Understanding the Full Return Picture

If you’re looking at that sample analysis thinking, “Negative cash flow? This is a terrible investment!”—hold on. This is where many beginners make a critical mistake. Real estate returns come from multiple sources, and cash flow is only one piece of the puzzle. Principal Paydown: Every monthly mortgage payment includes both interest (expense) and principal (equity building). In the example above, your tenants are paying down approximately $8,000-$10,000 in principal in the first year alone. That’s wealth building even with negative cash flow. Market Appreciation: Portland’s historical data shows 130% appreciation over 10 years—about 8.7% per year on a compound basis. If that trend continues (and the UGB suggests it will), your $700,000 property could be worth roughly $800,000 in just five years. That’s $100,000 in equity gain. Tax Advantages: The IRS allows rental property owners significant deductions:

- Operating expenses (property management, repairs, insurance, etc.)

- Mortgage interest

- Property taxes

- Depreciation (a non-cash expense that reduces taxable income)

Depreciation alone can create “paper losses” that offset your W-2 income (up to certain limits), reducing your overall tax burden. Consult a CPA familiar with real estate investing to maximize these benefits.

💡 Key Insight: When you combine principal paydown ($8,000), appreciation (potentially $40,000+ annually in strong years), and tax savings (variable), the “negative cash flow” of $15,000 looks very different. Many sophisticated investors willingly accept negative cash flow in high-appreciation markets because the total return far exceeds what they’d earn from cash flow alone.

Step 5: Risk Mitigation

Every investment carries risk. The question isn’t whether to take risks—it’s how to manage them intelligently. Budget for Vacancy: Even in Portland’s tight rental market, vacancy happens. Budget for at least 5% vacancy annually (roughly one month). This means in your financial projections, reduce your gross annual rental income by 5% before calculating NOI. Capital Expenditures (CapEx) Reserve: Major systems—roofs, HVAC, water heaters, appliances—don’t last forever. Set aside 5-10% of gross rental income for eventual replacement of these big-ticket items. If you collect $45,600 in annual rent, that’s $2,280-$4,560 per year into a CapEx fund. Tenant Screening: Your tenant is your customer and your business partner. Bad tenants can destroy your returns through late payments, property damage, and legal costs. Implement a thorough screening process that includes:

- Credit checks

- Income verification (many investors look for income 3x the rent)

- Rental history references

- Criminal background checks (while adhering to Portland’s FAIR ordinance limitations)

Professional Property Management: If you’re not experienced with property management, hiring a professional company (8-10% of gross rents) can actually save you money by reducing vacancy, handling maintenance efficiently, and ensuring legal compliance.

Know Before You Invest: Portland’s Tenant-Friendly Laws and What They Mean for You

Portland and Oregon have some of the most stringent landlord-tenant laws in the United States. While these regulations protect renters and promote housing stability, they also require landlords to operate with careful attention to compliance. Ignorance of these laws is not a defense—violations can result in significant financial penalties and legal liability.

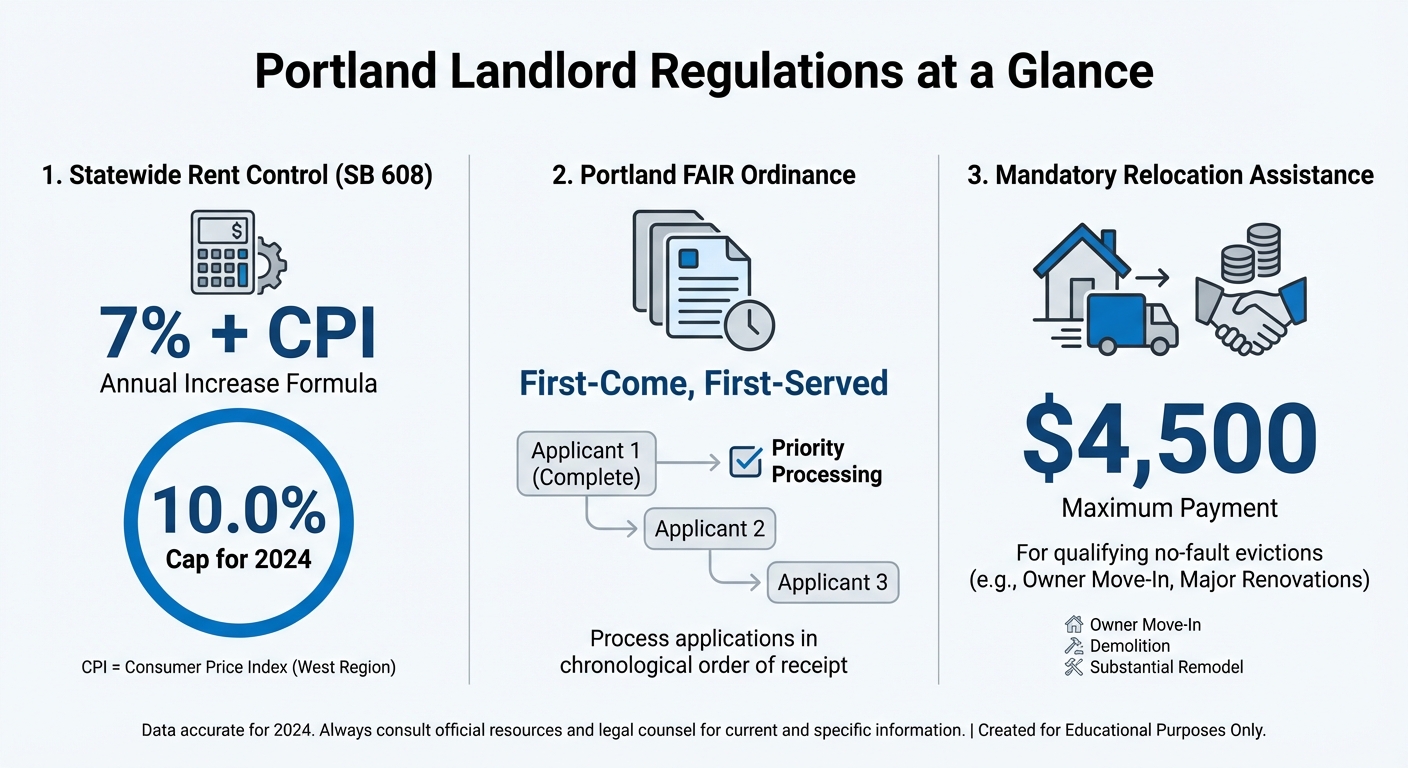

Oregon Senate Bill 608: Statewide Rent Control

Passed in 2019, Senate Bill 608 fundamentally changed the rules for rental housing across Oregon. This was groundbreaking legislation—Oregon became the first state to implement statewide rent control. Annual Rent Increase Cap: Landlords can increase rent once per year, but the increase cannot exceed 7% plus the Consumer Price Index. The specific percentage is published annually by the Oregon Office of Economic Analysis. For 2024, the maximum allowable increase was set at 10.0%. This means if you have a tenant paying $1,800/month, the most you could increase their rent in a single year is $180 (to $1,980/month), assuming the 10% cap applies. No-Cause Eviction Restrictions: After a tenant has occupied a unit for one year, landlords can no longer terminate the tenancy without cause. If you need to end a tenancy, you must provide a qualifying reason, such as:

- The owner or owner’s immediate family member intends to occupy the unit

- The property will be demolished or converted to non-residential use

- Major renovation that requires the unit to be vacant

For qualifying no-fault terminations, landlords may be required to pay relocation assistance to the tenant—a topic we’ll cover in the next section.

⚠️ Investment Implications: Rent control limits your ability to adjust rents to market rates if you acquire a property with below-market tenants. No-cause restrictions mean you can’t simply decide to “upgrade” your tenant pool without qualifying reasons. These are permanent features of the Oregon market—factor them into your underwriting and expect them to remain.

Portland’s FAIR Ordinance (Fair Access in Renting)

The City of Portland enacted the FAIR ordinance to regulate how landlords screen and select tenants. This is one of the most complex areas of Portland landlord-tenant law, and compliance is strictly enforced. First-Come, First-Served Application Processing: When you advertise a rental, you must accept applications and process them in the exact order received. You cannot “cherry-pick” applicants or hold applications hoping for better candidates. Practically, this means:

- Time-stamp every application when received

- Process the first application completely before moving to the second

- If the first applicant meets your criteria, you must offer them the unit

Screening Criteria Requirements: The FAIR ordinance mandates that landlords must either:

- Use “low-barrier” screening criteria (which are very permissive), or

- Conduct an “individual assessment” if an applicant doesn’t meet standard criteria

Low-Barrier Standards might include:

- No criminal history disqualifications (with limited exceptions for serious violent crimes or sex offenses)

- Very lenient credit score requirements

- Accepting alternative income verification for non-traditional workers

If you choose to use more restrictive criteria, you must conduct an individual assessment that considers:

- The relevance of the applicant’s history to their likelihood of being a successful tenant

- Evidence of rehabilitation or changed circumstances

- Positive rental history despite past issues

Criminal and Credit History Limitations: The ordinance severely restricts what criminal history or credit issues can be used to deny an applicant. Landlords cannot deny based on:

- Arrests that didn’t lead to convictions

- Criminal records older than 3-7 years (depending on the severity)

- Certain credit issues if the applicant can demonstrate financial stability through other means

⚠️ Compliance is Non-Negotiable: Portland’s FAIR ordinance is complex and strictly enforced. Violations can result in fines and legal liability. Many Portland landlords work with attorneys or property management companies who specialize in FAIR compliance to ensure they’re operating legally.

Additional Financial Obligations

Beyond rent control and screening regulations, Portland imposes several financial requirements that can significantly impact your bottom line. Mandatory Relocation Assistance: For qualifying no-fault evictions or certain rent increases that exceed the annual cap, landlords must pay relocation assistance to tenants:

- $2,900 for studio apartments

- $3,300 for 1-bedroom units

- $4,500 for 2-bedroom units

- $5,200 for 3+ bedroom units

These amounts are substantial and must be paid before the tenant moves out. Factor this potential cost into your exit strategy if you ever plan to:

- Move into the property yourself

- Renovate and re-position the property

- Convert the property to a different use

Security Deposit Limits: Oregon law caps security deposits at one month’s rent, but Portland adds an additional layer. If you collect last month’s rent in addition to a security deposit, the total cannot exceed 1.5 times the monthly rent. Additionally, you must:

- Provide detailed, itemized accounting for any deductions

- Return deposits (with accounting) within 31 days of move-out

- Pay interest on deposits held longer than one year (at a rate tied to the average savings account rate)

The Bottom Line for Investors

Portland’s regulatory environment is not going to change—if anything, it’s likely to become more tenant-friendly over time. This is not a reason to avoid investing in Portland; it’s simply the reality of the market that must be factored into your strategy.

How to Succeed:

- Educate yourself thoroughly on landlord-tenant law before making your first purchase

- Work with professionals who specialize in Portland rentals (property managers, real estate attorneys)

- Build compliance into your systems from day one—don’t try to cut corners

- View ethical, legal operation as a competitive advantage: Properties managed well, with quality tenants and full legal compliance, outperform in the long run

Ready to Begin? Your Actionable Next Steps for Portland Real Estate Success

You now understand Portland’s market fundamentals, the investment strategies that work here, the step-by-step process, and the regulatory landscape. Knowledge is the foundation—but action is what builds wealth. Here’s exactly what to do next.

Immediate Actions (This Week)

Deepen Your Education:

- Read summaries of Oregon’s landlord-tenant law

- Review Portland’s Bureau of Development Services resources on ADUs if that strategy interests you

- Join online communities of Portland real estate investors (BiggerPockets has active Portland forums)

Start Running Numbers:

- Open Zillow, Redfin, or Realtor.com and search for duplexes, triplexes, or fourplexes in Portland

- Use the financial analysis framework from this guide to evaluate properties

- Calculate NOI, cap rates, and cash-on-cash returns for at least 5 properties to build pattern recognition

Begin Networking:

- Search for Portland-area real estate investment associations (REIA groups)

- Attend a local real estate investing meetup

- Start connecting with investment-focused real estate agents on LinkedIn or through referrals

Short-Term Goals (This Month)

Get Financially Prepared:

- Pull your credit report and score (annualcreditreport.com for free reports)

- Calculate how much you can afford for a down payment based on your savings and investment accounts

- Research FHA lenders if you’re planning to house hack

- Get mortgage pre-approval from at least one lender

Define Your Strategy:

- Based on your available capital, risk tolerance, and time availability, choose your primary strategy:

- House hacking for minimal down payment and hands-on experience

- ADU development if you have equity in an existing property

- Traditional rental if you have 20-25% down payment saved

- Narrow your target neighborhoods based on your strategy and budget

Interview Team Members:

- Schedule calls with 2-3 real estate agents who specialize in investment properties

- Ask about their experience with multifamily transactions, rental comps knowledge, and off-market deal flow

- Talk to mortgage brokers about loan products and pre-approval requirements

Medium-Term Objectives (Next 3-6 Months)

Analyze Properties Systematically:

- Commit to analyzing 10-20 properties in detail

- Create a spreadsheet to track your analysis (purchase price, estimated rents, operating expenses, NOI, returns)

- This exercise builds confidence and helps you recognize good deals when they appear

Attend Property Inspections:

- Even if you don’t plan to make offers yet, ask your agent if you can attend inspections on properties they’re showing to other clients

- Learn what inspectors look for and how to spot red flags

Make Your First Offer:

- With your team in place, financing secured, and a clear understanding of what constitutes a good deal, submit an offer

- Don’t expect your first offer to be accepted—this is part of the process

- Each offer helps you refine your approach and understand how negotiations work

Mindset Shifts for Success

Essential Mindset Principles:

- Knowledge Reduces Risk: Every hour you spend learning about Portland’s market, running property analyses, and understanding regulations is an investment in your success. Informed decisions aren’t risk-free, but they drastically improve your odds.

- No Investment is Risk-Free: Every investment—real estate, stocks, bonds, starting a business—carries risk. The question isn’t whether to take risks but how to take intelligent, calculated risks with favorable risk/reward ratios.

- Adopt a Long-Term Perspective: Portland’s appreciation history (130% over 10 years) rewards patient, strategic investors. Don’t chase short-term gains or get discouraged by temporary market slowdowns. Real estate wealth is built over years and decades, not months.

- Take Action, But Don’t Rush: The biggest mistake new investors make is paralysis by analysis—studying forever but never taking action. The second-biggest mistake is rushing into a bad deal without proper due diligence. Find the balance: move deliberately but keep moving.

Connect with Local Expertise

While this guide provides a comprehensive foundation, every investor’s situation is unique. If you’re serious about making your first Portland investment, consider connecting with G.W. Hartley IV, a licensed Oregon broker since 1996 with nearly 30 years of experience in the Portland market. As a Top Producer affiliated with John L. Scott Real Estate, G.W. specializes in investment properties throughout the Portland metro area and can provide personalized guidance tailored to your specific goals, financial situation, and risk tolerance. Local expertise can help you avoid costly mistakes and identify opportunities that aren’t obvious to outsiders.

Ready to Take the Next Step?

Whether you’re looking for your first investment property or expanding your Portland portfolio, expert guidance makes all the difference.

Final Thoughts

Portland’s real estate market presents a compelling opportunity for beginners willing to approach it with discipline, education, and a long-term mindset. The combination of strong economic fundamentals (3.9% unemployment, steady population growth, diverse economy), a healthy rental market (4.4% vacancy rate, strong rent levels), and unique urban planning through the Urban Growth Boundary creates an environment where patient, strategic investors can build substantial wealth. Yes, the regulatory landscape is complex. Statewide rent control, Portland’s FAIR ordinance, mandatory relocation assistance, and strict security deposit rules require careful attention. But these are known, manageable factors—not insurmountable obstacles. Thousands of investors succeed in Portland every year by treating compliance as a business requirement and building ethical, legal operations from day one. Remember: real estate returns don’t come from cash flow alone. Principal paydown, market appreciation, and tax advantages combine to create wealth over time. A property that shows negative cash flow in year one may deliver a total return of 15-20% annually when you account for all components. This is why sophisticated investors focus on the complete picture rather than fixating on monthly cash flow. Your first investment is the hardest because it requires overcoming inertia and the fear of the unknown. But by following this evidence-based framework—understanding the market, choosing an appropriate strategy, systematically analyzing deals, building a professional team, and respecting the regulatory environment—you position yourself to make informed decisions with confidence. The journey begins with a single step: financial preparation, education, and strategic planning. Portland’s real estate market rewards those who approach it with knowledge, patience, and a long-term vision. The question isn’t whether you can succeed as a Portland real estate investor—it’s whether you’re willing to commit to the process of learning, planning, and taking intelligent action. Your wealth-building journey in the Rose City starts now.

References

- U.S. Census Bureau. (2024). Metropolitan and Micropolitan Statistical Areas Population Totals and Components of Change: 2020-2023. https://www.census.gov/data/tables/time-series/demo/popest/2020s-total-metro-and-micro-statistical-areas.html

- U.S. Bureau of Labor Statistics. (2024). Local Area Unemployment Statistics: Portland-Vancouver-Hillsboro, OR-WA. https://data.bls.gov/timeseries/LAUMT413890000000003

- Regional Multiple Listing Service (RMLS). (2024, November). Market Action, October 2024. https://www.rmlsweb.com/v2/public/marketAction/MA-Portland.pdf

- Multifamily NW. (2023). Fall 2023 Apartment Report. https://www.multifamilynw.org/advocacy/apartment-report

- U.S. Department of Housing and Urban Development (HUD). (n.d.). Let FHA Loans Help You. https://www.hud.gov/buying/loans

- City of Portland, Bureau of Development Services. (n.d.). Accessory Dwelling Units (ADUs). https://www.portland.gov/bds/zoning-land-use/zoning-districts/accessory-dwelling-units-adus

- Attom Data Solutions. (2021). Homes with Accessory Dwelling Units Command 35 Percent Sales Price Premium. https://www.attomdata.com/news/market-trends/home-sales-prices/attom-adu-sales-analysis/

- Oregon State Legislature. (2019). Senate Bill 608. https://olis.oregonlegislature.gov/liz/2019R1/Measures/Overview/SB608

- Oregon Office of Economic Analysis. (2023, September 13). Maximum Annual Rent Increase For 2024. https://oregoneconomicanalysis.com/2023/09/13/maximum-annual-rent-increase-for-2024/

- The City of Portland, Oregon. (n.d.). Fair Access in Renting (FAIR) Ordinances. https://www.portland.gov/phb/rental-services/fair-access-renting-fair-ordinances

- Federal Reserve Bank of St. Louis. (2024). All-Transactions House Price Index for Portland-Vancouver-Hillsboro, OR-WA (MSA). https://fred.stlouisfed.org/series/ATNHPIUS38900Q

- Oregon Metro. (n.d.). Urban growth boundary. https://www.oregonmetro.gov/urban-growth-boundary

- Internal Revenue Service (IRS). (2023). Publication 527, Residential Rental Property. https://www.irs.gov/publications/p527

- The City of Portland, Oregon. (n.d.). Mandatory Renter Relocation Assistance. https://www.portland.gov/phb/rental-services/renter-relocation-assistance

- The City of Portland, Oregon. (n.d.). Security Deposits. https://www.portland.gov/phb/rental-services/security-deposits