Table of Contents

The Portland, Oregon real estate market is no stranger to intense competition. With limited housing inventory, sustained buyer demand, and the region’s enduring appeal, multiple-offer scenarios—commonly known as “bidding wars”—have become the norm rather than the exception. For prospective homebuyers, this reality can feel daunting, stressful, and often overwhelming. But here’s the truth: winning in a competitive market isn’t just about offering the highest price. It requires a strategic, multi-faceted approach that addresses sellers’ deepest concerns—certainty, speed, and convenience—while managing your own financial risk. Consider this: In October 2023, Portland’s housing inventory sat at just 2.6 months of supply—well below the 4-6 months considered a balanced market. During peak competitive periods, that number has dropped below 1.5 months, with homes routinely selling within days of listing. Meanwhile, nearly two-thirds of current homeowners hold mortgage rates below 4%, creating a “lock-in effect” that further constrains available inventory. In this comprehensive guide, we’ll break down the proven strategies that can help you stand out in a sea of offers—from leveraging financial strength and strategically modifying contingencies to understanding escalation clauses and the pivotal role of expert representation. Whether you’re a first-time buyer or a seasoned investor, these insights will equip you to navigate Portland’s competitive market with confidence.

The Forces Driving Multiple-Offer Scenarios

Before crafting a winning offer, it’s essential to understand why Portland’s market is so competitive. The conditions creating bidding wars aren’t random—they’re the result of structural imbalances and persistent market forces that favor sellers.

Supply and Demand Imbalance

Portland’s competitive market is fundamentally driven by a chronic shortage of available homes. The city’s geographic growth boundaries, designed to preserve farmland and prevent urban sprawl, naturally limit development opportunities. When you combine this with limited new construction and persistent in-migration from people drawn to Portland’s culture, economy, and lifestyle, you create a structural shortage that consistently favors sellers. The situation has been exacerbated by what economists call the “mortgage rate lock-in effect.” Nearly 66% of homeowners in the region hold mortgages with interest rates below 4%. With current rates significantly higher, these homeowners face a powerful disincentive to sell—why give up a 3.5% mortgage to purchase a new home at 7%? This dynamic has artificially constrained the supply of homes available for sale, intensifying competition for what little inventory exists.

Critical Market Metrics

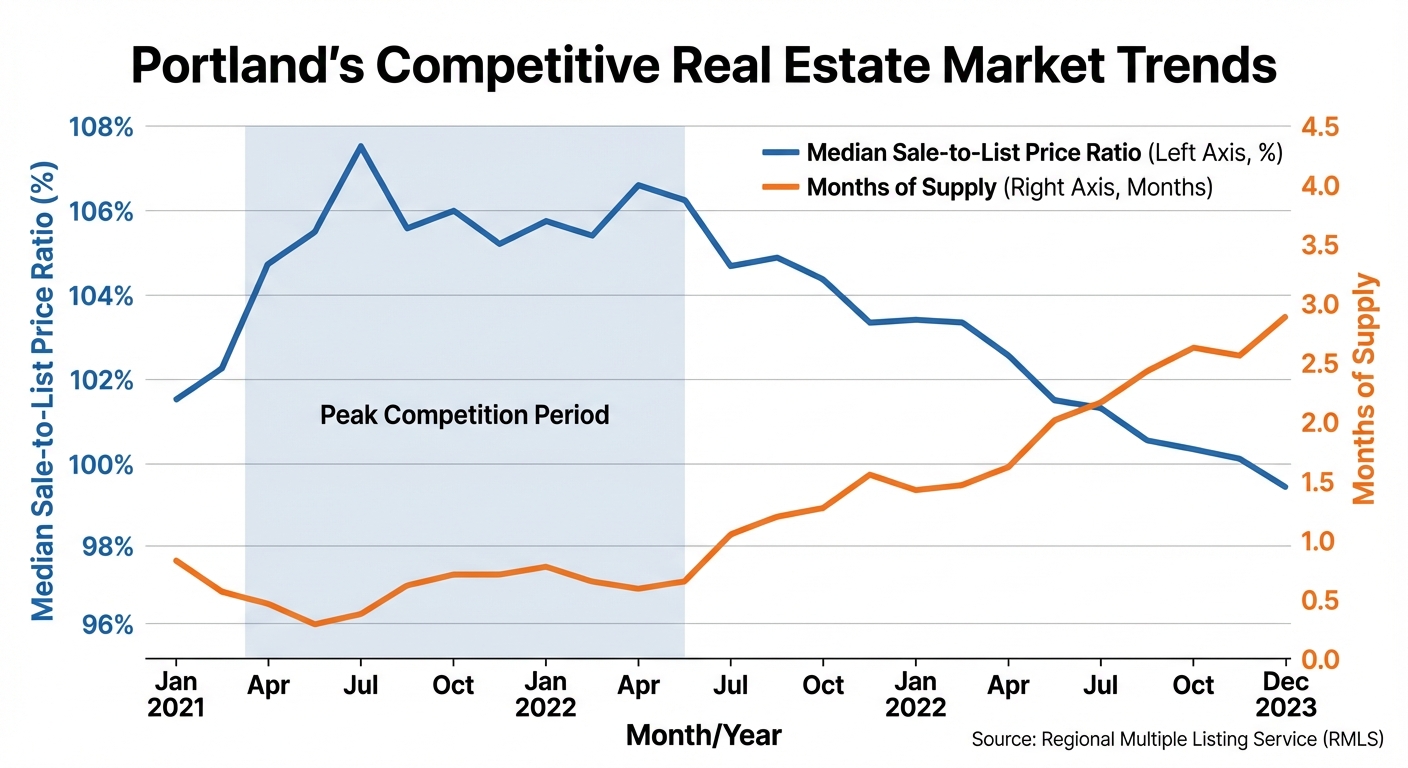

Understanding the numbers behind Portland’s market conditions helps buyers recognize what they’re up against: Inventory Levels: At 2.6 months of supply in October 2023, Portland remains firmly in seller’s market territory. Real estate professionals consider 4-6 months of inventory to represent a balanced market. Anything below 4 months tips the scales in favor of sellers, and Portland has consistently hovered in the 2-3 month range—sometimes dropping below 1.5 months during peak competition periods. Sale-to-List Price Ratio: This metric reveals how close final sale prices come to asking prices. While the October 2023 average was 97.9%, this figure masks the reality for desirable properties in sought-after neighborhoods. During the height of the 2021-2022 market surge, the market-wide ratio frequently exceeded 103%, with particularly attractive properties selling for 110-120% of list price. Even in more moderate periods, the best homes routinely command full asking price or more. Days on Market: The median cumulative days on market was 29 days in October 2023, but this average doesn’t tell the full story. During intense competition, properties often accept offers within a single weekend—sometimes in under 10 days. For buyers, this means being prepared to move quickly when the right property appears.

| Metric | Data Point | Market Indication |

|---|---|---|

| Months of Supply | 2.6 months | Seller’s Market |

| Median Sale Price | $525,000 | High Demand |

| Avg. Sale-to-List Ratio | 97.9% | Near Asking Price |

| Median Days on Market | 29 days | Fast-Paced |

Source: Regional Multiple Listing Service (RMLS) – October 2023

Seasonality and Timing

Portland’s real estate market follows predictable seasonal patterns, with spring and summer months typically seeing the highest buyer activity. Families prefer to move during school breaks, and the region’s notoriously rainy winters discourage house hunting for many. Understanding these cycles can help buyers time their search strategically—though in a persistently competitive market, waiting for a “better” time often means watching inventory shrink even further.

Proving You’re the Buyer Who Will Actually Close

In a multiple-offer situation, sellers prioritize one thing above all else: certainty. They want to know that the buyer who wins their home will actually make it to the closing table without drama, delays, or deal-killing surprises. Demonstrating overwhelming financial strength isn’t just about proving you can afford the home—it’s about eliminating the seller’s fear that your offer will fall apart.

Pre-Approval vs. Pre-Qualification

Many buyers mistakenly believe that a pre-qualification letter from their lender is sufficient. It’s not. A pre-qualification is merely a superficial estimate based on information you’ve provided verbally—it carries little weight because the lender hasn’t verified anything. A pre-approval, by contrast, is a conditional commitment based on a verified review of your income, assets, and credit history. The lender has pulled your credit report, examined your tax returns and pay stubs, and verified your down payment funds. This document tells the seller that a professional has scrutinized your finances and determined you’re qualified to borrow the necessary funds. But there’s an even stronger option: TBD (To Be Determined) approval, where you’ve completed full underwriting upfront. In this scenario, the lender has approved everything except the property itself. Only the appraisal and title review remain. This level of preparation allows you to potentially waive your financing contingency with genuine confidence, making your financed offer nearly as strong as cash. Working with a reputable local lender whose name carries weight with Portland listing agents can also provide a subtle advantage. Agents know which lenders are thorough, responsive, and reliable—and they advise their clients accordingly.

Earnest Money That Signals Seriousness

Earnest money is your good-faith deposit, demonstrating that you’re a serious buyer willing to put substantial funds at risk. While typical deposits range from 1-3% of the sale price, with a median of 2% nationally, offering significantly more immediately sets you apart. Consider the psychological impact: On a $700,000 home, a 2% earnest money deposit equals $14,000—standard and unremarkable. But a 5% deposit equals $35,000. That extra $21,000 sends a powerful message about your financial capability and commitment. It tells the seller you have substantial liquid assets and you’re willing to put them on the line because you’re confident in your ability to close.

Proof of Funds Documentation

Transparency builds trust. Providing redacted bank statements or letters from your financial institution proving you have cash readily available eliminates seller concerns about your ability to perform. Specifically, you should demonstrate funds for:

- Your down payment

- Closing costs

- Any potential appraisal gap coverage (more on this shortly)

This documentation transforms your offer from a promise into a demonstrable reality.

The Cash Offer Advantage

Nationally, 28% of all home sales in 2023 were all-cash transactions. In Portland’s competitive market, that percentage can be even higher for certain property types and price points. Cash offers eliminate both financing and appraisal contingencies—the two biggest deal-killers that keep sellers awake at night. Most buyers can’t pay cash, of course. But understanding the overwhelming advantage cash provides should inform your strategy: Your goal is to make your financed offer as secure and certain as a cash offer through the tactics outlined above.

💡 Key Insight:

89% of recent homebuyers used a real estate agent to guide them through this complex process, underscoring that professional expertise is critical when the stakes are this high.

The Art of Calculated Risk: Modifying Contingencies to Win

Contingencies are protective clauses that allow you to back out of a contract without penalty under specific circumstances. They protect buyers—but from the seller’s perspective, they represent uncertainty and potential paths for the deal to collapse. Understanding how to strategically modify or waive contingencies while managing your own risk is perhaps the most nuanced skill in competitive offer writing.

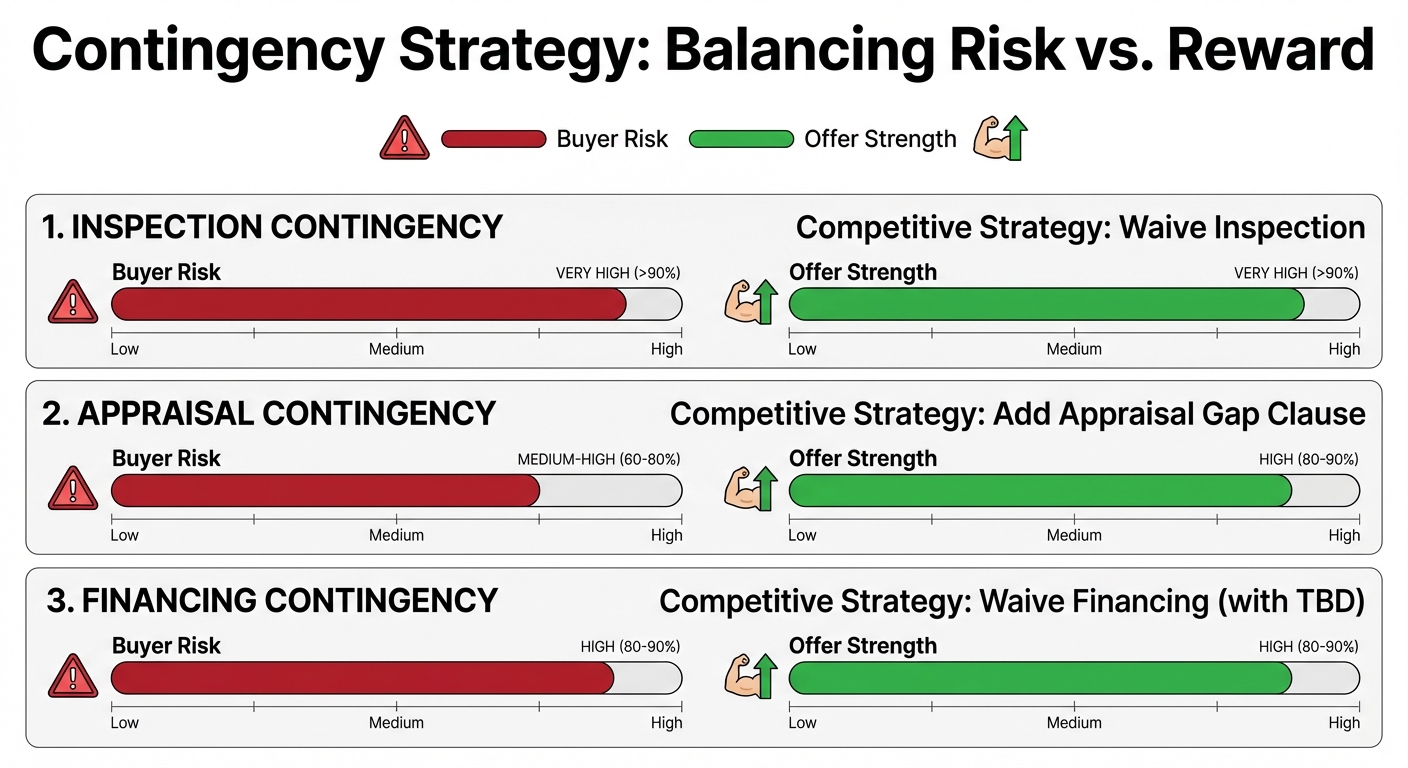

The Inspection Contingency

The standard inspection contingency gives buyers 10 business days to conduct professional home inspections and negotiate repairs or terminate the contract. In a competitive market, you can make your offer more attractive through several approaches: Shorten the timeline: Offer a 3-5 day inspection period instead of the standard 10. This demonstrates efficiency and signals you won’t drag out the process. Conduct a pre-inspection: If the seller allows it (and many do in competitive markets), hire an inspector before submitting your offer. This allows you to waive the inspection contingency entirely because you’ve already seen what you’re buying. The seller gains tremendous peace of mind knowing you’ve done your homework and won’t come back with a laundry list of demands. Use a “pass/fail” approach: Inform the seller you’ll only terminate the contract for major structural or safety issues, and you won’t negotiate for minor repairs. This strategy signals you understand that used homes aren’t perfect and you’re not looking to nickel-and-dime them over cosmetic concerns.

⚠️ Warning: The Nuclear Option

Waiving inspections entirely is extraordinarily risky and should only be considered when you truly understand and accept the potential for discovering costly, unknown defects with no recourse. Even a seemingly perfect home can harbor expensive surprises like foundation issues, hidden water damage, or failing systems.

The Appraisal Contingency

This contingency protects you if the home appraises for less than your offer price—a common concern when bidding wars push prices above the value an objective appraiser might assign. If the appraisal comes in low and you have this contingency, you can either renegotiate the price, increase your down payment to make up the difference, or walk away with your earnest money intact. In a competitive market, sellers worry intensely about low appraisals derailing the deal. You can address this fear with an appraisal gap clause—a written commitment to cover the difference between the appraised value and purchase price up to a specific dollar amount in cash.

Example Appraisal Gap Clause:

“Buyer will cover up to $25,000 of any appraisal gap in cash.”

This strategy directly targets the seller’s primary anxiety. Even if you’re offering $775,000 but the home appraises for $750,000, you’re guaranteeing the seller will receive the full $775,000. The catch? You must have that $25,000 available in liquid cash, separate from your down payment funds. The strategic question becomes: How large should your appraisal gap coverage be? Too small, and it doesn’t meaningfully reduce seller risk. Too large, and you’re making a promise you may not be able to keep. A good rule of thumb is 3-5% of the purchase price, though this varies by property and market conditions.

The Financing Contingency

This allows you to exit the contract if your loan falls through. In theory, if you have a solid pre-approval, this seems like a safe contingency to keep. In practice, removing it makes your offer substantially more compelling because it eliminates the seller’s fear that your lender will discover a problem at the last minute. Only waive this contingency if you have a fully underwritten pre-approval (TBD approval). Even then, understand the risk: If something unexpected happens—job loss, changes in your credit score, issues with the property that prevent it from meeting lending standards—you could lose your earnest money.

| Contingency | Competitive Strategy | Reward (Seller/Offer) | Risk (Buyer) |

|---|---|---|---|

| Inspection | Shorten period; pre-inspect; “pass/fail”; waive | Reduces uncertainty & speeds timeline | High: Unknown defects with no recourse |

| Appraisal | Waive or add gap clause | Guarantees full price regardless of appraisal | Moderate-High: Must cover gap in cash |

| Financing | Waive (with TBD approval only) | Eliminates loan-failure risk | High: Could lose earnest money if loan fails |

The Key Insight:

Every contingency you modify or remove increases seller confidence—but also your financial exposure. Work with your agent to find the right balance for your specific situation and risk tolerance.

Going Beyond the Basics: Escalation Clauses and the “Bully Offer”

For buyers willing to employ more aggressive tactics, escalation clauses and preemptive offers can be game-changers—but they require careful execution and a clear understanding of their strengths and weaknesses.

The Escalation Clause Explained

An escalation clause is an addendum stating you’ll pay a certain amount above the highest competing offer, up to a maximum price. Here’s how it works:

“Buyer offers $750,000. If Seller receives a bona fide competing offer, Buyer agrees to increase the price to $2,500 above the competing offer, up to a maximum of $785,000.”

The appeal: You don’t immediately reveal your absolute maximum, and you create an automated mechanism to ensure you’re the highest bidder within your budget. If the next-highest offer is $760,000, your escalation clause automatically bumps you to $762,500. If it’s $780,000, you’re at your cap of $785,000. The challenge: The escalation clause reveals your top price to the seller from the outset. In a scenario where the seller counters all buyers (which happens frequently), they may simply counter you at your $785,000 maximum, regardless of what other offers actually stated.

Best Practices for Escalation Clauses

If you choose to use an escalation clause, protect yourself with these requirements: Demand to see the competing offer: Your clause must require the seller to provide a complete, unredacted copy of the bona fide competing offer that triggered your escalation. Without this provision, you have no way to verify that the escalation was legitimate. Strategic increment amounts: Your escalation increment—the amount you beat the other offer by—matters. A $1,000 increment might be insufficient to make a psychological impact. Consider $2,500 to $5,000 increments that clearly differentiate your offer while not unnecessarily inflating your price. Price your maximum carefully: Your cap should represent the absolute most you’re willing to pay, but recognize that there’s a good chance you’ll end up at that number. Don’t set a maximum you’ll regret.

The Preemptive (“Bully”) Offer

A preemptive offer—sometimes called a “bully offer”—is submitted before the seller’s designated offer review date with an extremely short expiration (typically 12-24 hours). The strategy is to present an offer so compelling that the seller accepts immediately and cancels their planned review of other offers. Requirements for success: A preemptive offer must be exceptional in both price and terms. You’re asking the seller to forgo the opportunity to see what else the market might bring, so you must make it worth their while. This typically means:

- Offering well above the list price

- Minimal or no contingencies

- Favorable terms (flexible closing, rent-back if needed)

- Strong financial documentation

The risk: If your offer isn’t strong enough, you’ve shown your hand early and potentially set a high bar for the official offer review. Some listing agents will use a weak preemptive offer to generate even more interest: “We already have an offer of $X, so bring your best.” When it works: Preemptive offers are most effective when the seller values certainty over maximizing price, or when market timing creates urgency (perhaps they’re already under contract on their next home). It’s a high-risk, high-reward strategy that can eliminate competition entirely—but it can also backfire if not executed with precision.

Why Your Agent Is Your Secret Weapon (And What to Avoid)

In a multiple-offer scenario, the skill and reputation of your real estate agent often becomes the deciding factor. While buyers might focus on the written terms of their offer, the relationship and communication between agents can create advantages that are invisible on paper but profound in impact.

Intelligence Gathering

An experienced local agent’s greatest value often lies in what they can learn before you even write your offer. Through professional communication with the listing agent, a skilled buyer’s agent can uncover critical intelligence: What matters most to the sellers beyond price? Perhaps they need a 45-day closing to coordinate with their next purchase. Maybe they require a two-week rent-back period to avoid moving twice. Some sellers prioritize a clean, simple transaction over squeezing every dollar out of the sale. Are they concerned about the appraisal? If the sellers or their agent express this worry, it tells you that an appraisal gap clause will carry extra weight. How many offers are expected? Understanding the level of competition helps you calibrate your strategy. Facing 2-3 offers calls for different tactics than competing against 15. Are there any property issues to be aware of? Sometimes listing agents will candidly share information about known issues—a roof that’s near the end of its life, a basement that’s had minor water intrusion, outdated electrical systems. This transparency allows you to make informed decisions about inspections. This intelligence gathering allows you to tailor your offer to address the seller’s specific, non-financial motivations—often the difference between being chosen and being passed over.

The Reputation Factor

In Portland’s tight-knit real estate community, agent reputations matter enormously. When a listing agent receives multiple offers and several are financially similar, they’ll often advise their clients to favor the offer from an agent known for professionalism, thoroughness, and the ability to close deals smoothly. Why? Because an agent’s reputation signals the likelihood of a successful closing. Agents who consistently dot every “i” and cross every “t,” who return calls promptly, who anticipate problems before they arise, and who maintain composure during stressful negotiations create confidence. A listing agent knows that choosing an offer from a respected buyer’s agent reduces their own liability and stress. This “soft” advantage can tip the scales when offers are close in price and terms. It’s invisible in the contract but invaluable in practice.

Structuring Excellence

Expert agents understand the psychology and mechanics of offer presentation: Document preparation: A clean, easy-to-read offer package with all required documentation properly organized makes a psychological impression. When a seller reviews twelve offers, the one that’s professionally assembled and instantly understandable has a subtle advantage. Strategic timing: Submitting your offer slightly before the deadline (not at the last minute) can signal confidence and preparedness. Escalation clause calibration: An experienced agent knows what escalation increments are appropriate for different price points and market conditions in Portland’s various neighborhoods. Communication style: How your agent communicates with the listing agent matters. Professional courtesy, responsiveness, and clarity build bridges.

The “Love Letter” Legal Minefield

For years, buyer “love letters”—personal letters to sellers explaining why you’re the perfect family for their home—were a popular tactic. Today, they represent a significant legal liability and should be avoided entirely. The Fair Housing Act prohibits discrimination based on race, religion, color, national origin, sex, familial status, and disability. Personal letters almost inevitably reveal protected characteristics—photos of your family, mentions of your children, references to your church or community involvement, descriptions of your background. In 2021, Oregon passed House Bill 2550, directing real estate licensees to reject such letters to avoid potential fair housing violations. While a federal court later found this law to be an unconstitutional restriction on free speech, the underlying legal risk for sellers remains very real. If a seller accepts one offer over others, and rejected buyers believe the decision was influenced by discriminatory factors revealed in a love letter, the seller faces potential fair housing complaints and lawsuits. Reputable agents advise against love letters categorically. Instead, your agent should communicate your enthusiasm for the home and your strength as a buyer in professional, objective terms that don’t expose the seller to discrimination claims.

Bottom Line:

89% of recent homebuyers used a real estate agent, and in a competitive multiple-offer situation, that professional representation often determines success or failure. Choose your agent as carefully as you choose your home.

Key Takeaways

Winning in Portland’s competitive real estate market requires far more than simply offering the highest price. Success comes from a comprehensive, strategic approach that addresses sellers’ fundamental concerns—financial certainty, transaction speed, and convenience—while carefully managing your own risk exposure. The buyers who consistently succeed in multiple-offer situations are those who:

- ✅ Secure robust financing well in advance, ideally with full underwriting that allows them to compete almost as confidently as cash buyers

- ✅ Demonstrate overwhelming financial strength through substantial earnest money deposits and documented proof of funds that eliminate seller doubts

- ✅ Strategically modify contingencies after thoroughly understanding the associated risks, creating offers that provide sellers with certainty while maintaining appropriate buyer protections

- ✅ Employ advanced tactics like escalation clauses with proper safeguards and appraisal gap coverage that directly address seller anxieties about deal-killing surprises

- ✅ Leverage the market intelligence, professional reputation, and structural expertise of a skilled local agent who understands Portland’s unique market dynamics

Remember: The data tells a clear story. With inventory at just 2.6 months—well below the 4-6 months that defines a balanced market—and with 28% of homes purchased with cash nationally, Portland’s competitive environment rewards preparation and strategy above all else. Nearly two-thirds of current homeowners are locked into mortgages below 4%, creating an artificial constraint on supply that shows no signs of easing. This isn’t a market where hesitation, weak financing, or amateur-hour offer writing will succeed. But for buyers who approach the process with the strategies outlined in this guide, supported by expert representation, the dream of homeownership in Portland remains very achievable.

Ready to Develop Your Winning Strategy?

Connect with G.W. Hartley IV, an experienced Portland real estate professional who understands these dynamics and can guide you through every step of the competitive offer process. With the right preparation and expert guidance, your next offer could be the winning one.

References:

- Regional Multiple Listing Service (RMLS). (2023, November). Market Action Report, October 2023. Retrieved from https://www.rmls.com/reports/market-action

- Redfin Data Center. (2024). Portland, OR Housing Market Trends. Retrieved from https://www.redfin.com/city/15245/OR/Portland/housing-market

- Consumer Financial Protection Bureau (CFPB). (2020, April 16). What’s the difference between a mortgage prequalification and a preapproval? Retrieved from https://www.consumerfinance.gov/ask-cfpb/whats-the-difference-between-a-mortgage-prequalification-and-a-preapproval-en-122/

- National Association of REALTORS®. (2023). 2023 Profile of Home Buyers and Sellers. Retrieved from https://www.nar.realtor/research-and-statistics/research-reports/highlights-from-the-profile-of-home-buyers-and-sellers

- Consumer Financial Protection Bureau (CFPB). (2023). Home closing: What to expect. Retrieved from https://www.consumerfinance.gov/owning-a-home/closing/

- U.S. Department of Housing and Urban Development (HUD). Fair Housing Act. Retrieved from https://www.hud.gov/program_offices/fair_housing_equal_opp/fair_housing_act_overview

- National Association of REALTORS®. (2022, May 4). Court Issues Ruling on Oregon ‘Love Letter’ Law. Retrieved from https://www.nar.realtor/magazine/real-estate-news/law-and-ethics/court-issues-ruling-on-oregon-love-letter-law

- Federal Housing Finance Agency (FHFA). (2023). The Lock-In Effect of Rising Mortgage Rates. Retrieved from https://www.fhfa.gov/Policy-Research/Research/Pages/The-Lock-In-Effect-of-Rising-Mortgage-Rates.aspx

- The New York Times. (2021, April 23). The ‘Bully Offer’: A Tactic for Frustrated Home Buyers. Retrieved from https://www.nytimes.com/2021/04/23/realestate/bully-offer-real-estate.html