Table of Contents

- What You Need to Know About Portland’s Housing Market Right Now

- Where Can You Afford to Live? A Neighborhood-by-Neighborhood Breakdown

- The Money Talk: Credit, Down Payments, and Assistance Programs That Can Help

- From Offer to Keys: Navigating Oregon’s Unique Home Buying Process

- Let’s Talk About What You’re Really Worried About

- Final Thoughts

Buying your first home is one of life’s most significant milestones—a moment that symbolizes independence, stability, and the realization of the American Dream. But if you’re eyeing the Portland metropolitan area, you’ve probably discovered that this dream comes with a hefty price tag and a learning curve that can feel overwhelming.

With a median home price hovering around $550,000, Portland’s housing market presents real affordability challenges for first-time buyers. The inventory shortage, competitive offers, and complex financial requirements can make the process feel daunting. But here’s the truth: with strategic preparation and the right guidance, homeownership in Portland is absolutely achievable.

This comprehensive guide will walk you through everything you need to know—from understanding the current market dynamics and finding neighborhoods that fit your budget, to navigating Oregon’s unique home buying process and leveraging assistance programs designed specifically for first-time buyers. We’ve backed every recommendation with data from authoritative sources including the Regional Multiple Listing Service, the Federal Reserve, and Oregon state housing agencies.

Whether you’re wondering if now is the right time to buy, how to save for a down payment, or what happens during the closing process, this guide has you covered. Let’s transform that anxiety into confidence and get you on the path to homeownership.

What You Need to Know About Portland’s Housing Market Right Now

Before you start touring homes or calculating monthly payments, you need to understand the landscape you’re entering. Portland’s housing market has its own personality, shaped by unique geographic constraints, strong long-term demand, and economic factors that set it apart from other West Coast cities.

Current Market Snapshot (Early 2024)

The Portland metro housing market has cooled somewhat from its pandemic-era frenzy, but it remains competitive, particularly for well-priced homes in desirable neighborhoods. Here’s what the numbers tell us:

The median home sale price across the Portland metro area sits at approximately $550,000. However, this figure masks significant variation across the region’s three primary counties. Multnomah County (which includes Portland proper) shows a median around $575,000, while Washington County to the west commands approximately $600,000, and Clackamas County to the south comes in at roughly $580,000.

Homes are spending an average of 40-50 days on the market, a stark contrast to the mere days or hours of the 2021-2022 seller’s market. This represents a healthier, more balanced market where buyers have time to conduct proper due diligence without the intense pressure of instant bidding wars.

Properties are selling for approximately 98-99% of their original list price on average, indicating that while aggressive over-bidding has cooled, well-priced homes still command prices very close to asking value. The inventory situation remains tight at roughly 2-3 months of supply across the metro area—anything under six months is considered a seller’s market.

| County | Median Sale Price | Avg. Days on Market | Months of Inventory |

|---|---|---|---|

| Multnomah | ~$575,000 | ~45 Days | ~2.5 Months |

| Washington | ~$600,000 | ~40 Days | ~2.1 Months |

| Clackamas | ~$580,000 | ~50 Days | ~2.8 Months |

Historical Context: The Long View Matters

If you’re worried about buying at “the top of the market,” historical data provides valuable perspective. The Federal Reserve’s All-Transactions House Price Index for the Portland-Vancouver-Hillsboro metro area shows a consistent upward trajectory over the past two decades, with property values demonstrating remarkable resilience even through economic downturns.

This long-term appreciation is partly driven by Portland’s Urban Growth Boundary (UGB)—a land-use planning tool that restricts urban sprawl by creating a clear line between urban and rural land. While controversial, the UGB has effectively limited the supply of developable land within the metro area, supporting property values and preventing the kind of suburban sprawl common in other Western cities.

The key takeaway? Short-term market fluctuations are normal, but Portland real estate has proven to be a solid long-term investment for those who can afford the entry point and plan to stay put for at least five to seven years.

The Affordability Challenge: Let’s Be Honest

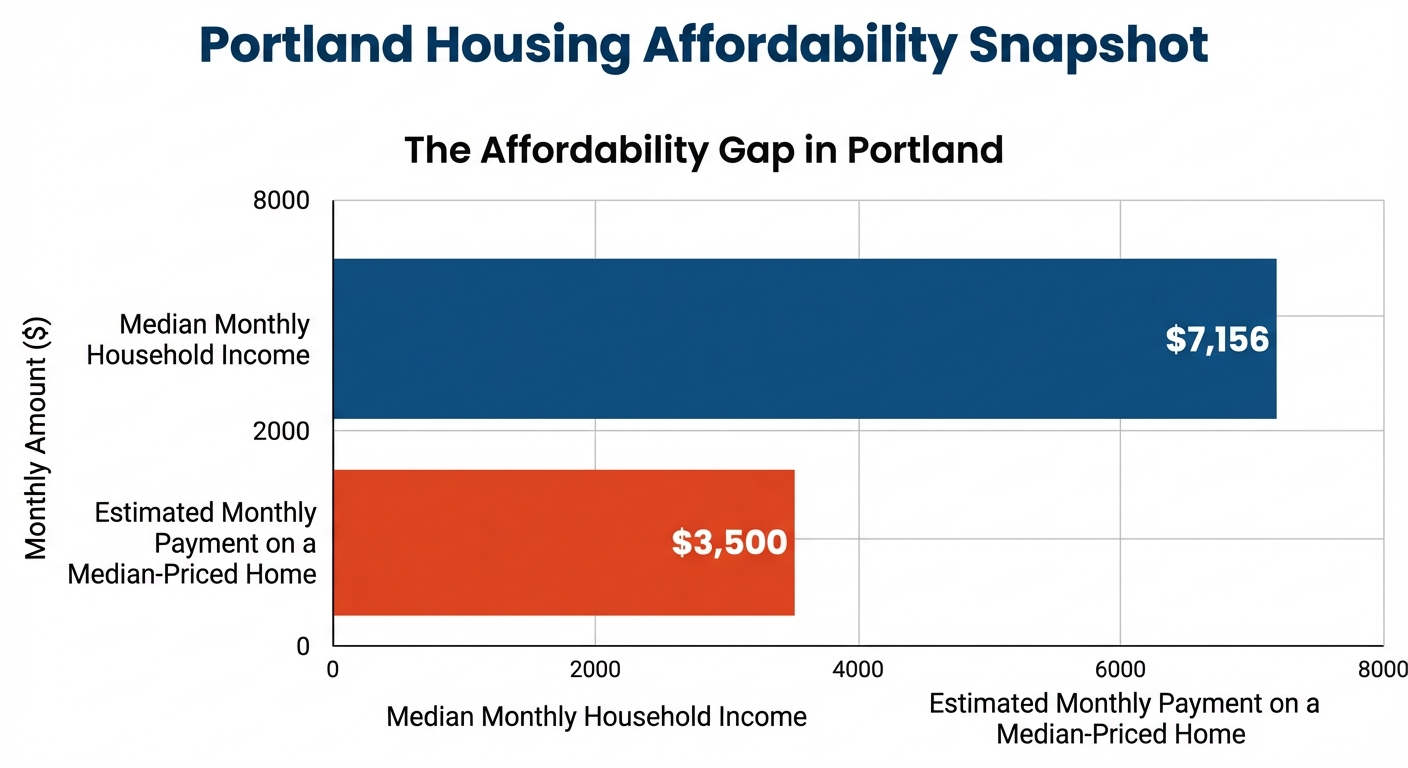

Portland’s housing market presents a significant affordability hurdle. The median household income in the Portland metro area is approximately $85,876. To purchase a $550,000 home with a 10% down payment ($55,000) at a 6.5% interest rate, you’re looking at a monthly payment exceeding $3,500 when you factor in principal, interest, property taxes, and insurance (PITI). That’s a substantial portion of the median household’s pre-tax income.

The down payment itself represents one of the most significant barriers. A 10% down payment on a median-priced home equals $55,000—a sum that takes years for many households to save, especially while paying high rental costs. According to the National Association of Realtors, 29% of first-time buyers cite the down payment as the most difficult step in the home buying process.

Oregon’s “housing wage”—the hourly wage a worker must earn to afford a modest two-bedroom rental apartment—stands at $29.71 per hour, far exceeding the state’s minimum wage. This reality underscores the broader affordability crisis and explains why saving for a down payment while renting can feel like running on a treadmill.

But here’s the good news: Understanding these challenges is the first step in overcoming them. Oregon offers specific assistance programs designed to help first-time buyers bridge this affordability gap, and we’ll explore those in detail later in this guide.

Where Can You Afford to Live? A Neighborhood-by-Neighborhood Breakdown

One of the most common misconceptions about the Portland market is treating it as a single entity. The reality? Portland is a collection of distinct micro-markets, each with its own character, price point, and lifestyle offerings. That $550,000 median price we discussed? It’s just an average—your actual options will vary dramatically depending on where you choose to plant roots.

Portland Is Not One Market—It’s Many

A home in Gresham presents a vastly different value proposition than one in Lake Oswego. East Portland offers different amenities than the trendy inner Southeast neighborhoods. Understanding these distinctions is critical to finding a home that fits both your budget and your lifestyle.

| Area/Neighborhood | Character | Median Sale Price |

|---|---|---|

| Beaverton (Washington Co.) | Suburban, Tech Corridor, Family-Friendly | $580,000 |

| Hillsboro (Washington Co.) | Tech Hub (“Silicon Forest”), Newer Developments | $550,000 |

| SE Portland (Multnomah Co.) | Eclectic, Walkable, Mix of Historic & New | $600,000 |

| N Portland (Multnomah Co.) | Diverse, Historic, Good Transit Access | $540,000 |

| Gresham (Multnomah Co.) | More Affordable Entry Point, Suburban, Nature Access | $485,000 |

| Lake Oswego (Clackamas Co.) | Affluent, Excellent Schools, Lakeside Living | $950,000+ |

| Oregon City (Clackamas Co.) | Historic, River Views, Growing Suburb | $560,000 |

Making the Right Location Choice

Price is just one factor in your neighborhood decision. Consider these additional elements:

Commute Times and Transit: Portland’s traffic congestion is real, but the city offers one of the West Coast’s better public transit systems (MAX light rail, buses, streetcar). If you’re commuting downtown or to the Silicon Forest tech corridor, proximity to transit can be a game-changer for your quality of life.

School Districts: If you have or plan to have children, school quality often becomes the primary location driver. Lake Oswego, West Linn, and parts of Beaverton command premium prices partly due to highly-rated schools.

Access to Nature: Portlanders take their outdoor recreation seriously. Proximity to Forest Park, the Columbia River Gorge, Mount Hood, or the Oregon Coast can significantly impact your lifestyle satisfaction.

Walkability and Neighborhood Amenities: Inner Portland neighborhoods like Hawthorne, Alberta, Mississippi, and Division offer walkable street life with independent shops, restaurants, and cultural venues. If car-free or car-lite living appeals to you, these areas deliver—but at a premium price.

Future Development: Research what’s in the pipeline for your target area. A new MAX line, major commercial development, or planned infrastructure improvements can signal future appreciation potential.

The right neighborhood isn’t just about what you can afford today—it’s about where you’ll be happy living for the next several years and which area offers the best long-term value proposition for your specific situation.

The Money Talk: Credit, Down Payments, and Assistance Programs That Can Help

Let’s address the elephant in the room: Can you actually afford to buy a home in Portland? The answer depends less on your current income and more on your strategic financial preparation. This section covers the critical financial components—credit management, debt ratios, down payment strategies, and the assistance programs specifically designed to help first-time Oregon buyers.

Credit & Debt Management: Your Financial Foundation

Your Credit Score Is Your Superpower

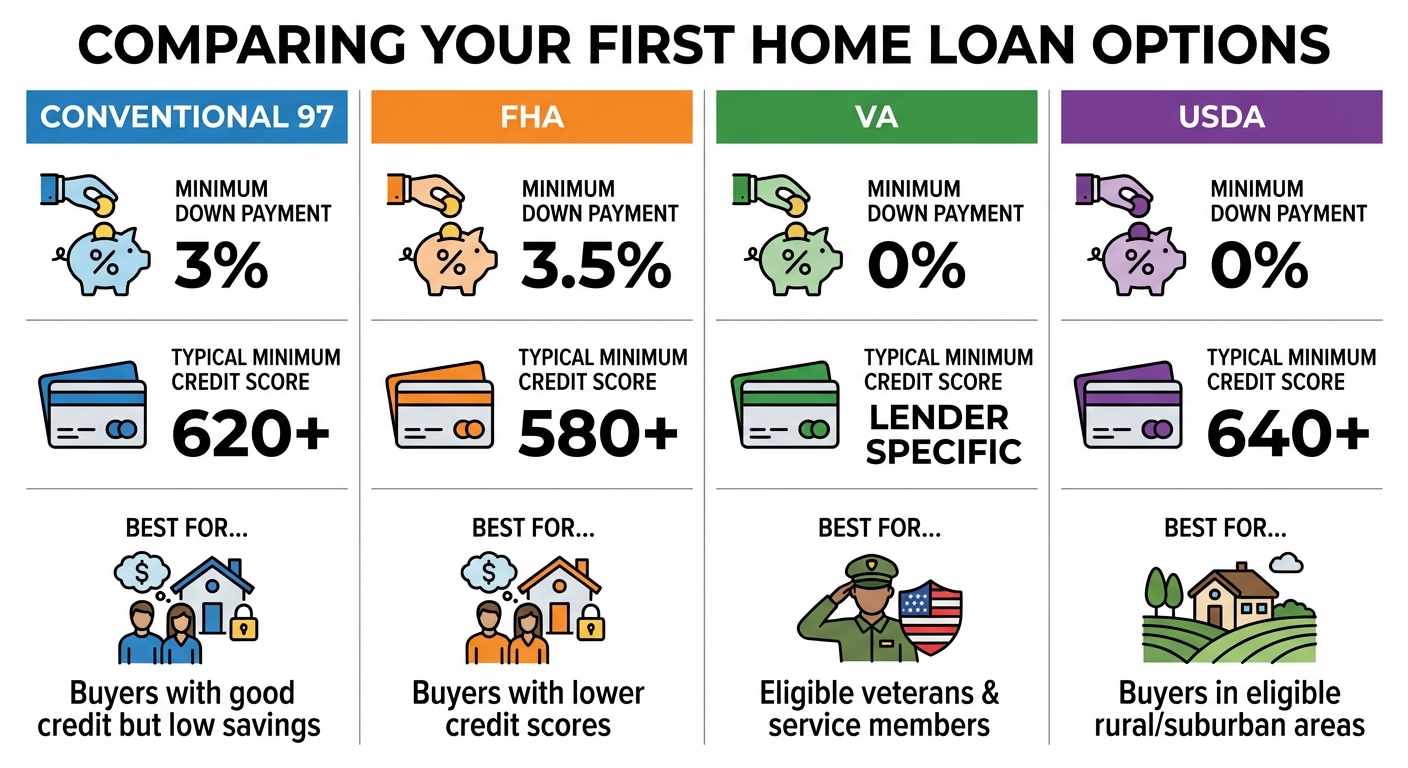

In the world of mortgage lending, your credit score functions as your financial reputation score. A credit score of 740 or higher typically unlocks the best interest rates available, potentially saving you tens of thousands of dollars over the life of your loan. However, many loan programs accept lower scores—FHA loans may approve borrowers with scores as low as 580, and conventional loans typically start at 620.

Here’s why this matters: Even a half-percentage-point difference in your interest rate can mean hundreds of dollars per month and tens of thousands over 30 years. Before house hunting, obtain free credit reports, dispute any errors, and strategically pay down high-interest debt to improve your score.

The Debt-to-Income (DTI) Ratio: Your Affordability Ceiling

Lenders use your DTI ratio to determine how much house you can afford. This ratio represents the percentage of your gross monthly income that goes toward paying monthly debt obligations—including your future mortgage payment, car loans, student loans, credit card minimum payments, and other recurring debts.

Most conventional lenders prefer a DTI of 43% or less, though some programs allow up to 50%. Calculate your DTI by dividing your total monthly debt payments by your gross monthly income. If your DTI is high, focus on paying down debt before applying for a mortgage—this strategy not only improves your approval odds but also qualifies you for better interest rates.

Down Payments & Closing Costs: The Reality and the Help Available

Down Payment Strategies

The traditional 20% down payment is not always necessary—in fact, many first-time buyers put down between 3% and 10%. The trade-off? A lower down payment typically means a higher monthly payment and the addition of private mortgage insurance (PMI) or mortgage insurance premiums, which protect the lender if you default.

Portland and Oregon Assistance Programs: Your Secret Weapon

Here’s where being a first-time buyer in Oregon becomes an advantage. The state and city have created specific programs to address the affordability crisis:

Oregon Bond Residential Loan Program: This state program offers competitive interest rates and down payment assistance to qualifying first-time home buyers. The program has income limits (which vary by county and household size) and purchase price limits, but for eligible buyers, it can provide crucial down payment support and a rate advantage.

Portland Down Payment Assistance Loan (DPAL): For buyers purchasing within Portland city limits, this program is a potential game-changer. DPAL can provide up to $100,000 in the form of a second mortgage loan to help with down payment and closing costs. The loan is typically structured as a deferred, silent second mortgage that becomes due when you sell the home, refinance, or no longer occupy it as your primary residence. Like the Bond program, DPAL has income and purchase price limits that buyers must meet.

These programs exist precisely because policymakers recognize the affordability challenges facing first-time buyers. Don’t leave this money on the table—work with a lender familiar with these programs to determine your eligibility.

Closing Costs: Budget for the Finish Line

Beyond your down payment, you’ll need to budget for closing costs, which typically range from 2% to 5% of the home’s purchase price. On a $550,000 home, that translates to approximately $11,000 to $27,500.

| Cost Item | Estimated Amount | Notes |

|---|---|---|

| Loan Origination Fee | $2,750 – $5,500 | Typically 0.5% – 1.0% of loan amount |

| Appraisal Fee | $600 – $900 | Confirms home’s value for lender |

| Title Insurance | $1,500 – $2,500 | Protects against title defects; often split |

| Escrow Fee | $1,000 – $2,000 | Neutral third party handling; often split |

| Home Inspection | $400 – $600 | Critical for due diligence |

| Prepaid Taxes & Insurance | $2,000 – $4,000 | Establishes escrow account |

| Recording Fees | $100 – $200 | County fee to record new deed |

| Total Estimated Range | $8,350 – $17,700+ | Actual costs detailed in Loan Estimate |

Federal regulations require your lender to provide a Loan Estimate within three business days of your loan application, breaking down all estimated costs in a standardized format. This transparency empowers you to shop lenders and understand exactly where your money is going.

Getting Pre-Approved: Your Competitive Edge

There’s a critical difference between pre-qualification and pre-approval. Pre-qualification is an informal estimate based on unverified information. Pre-approval means a lender has actually verified your income, assets, and credit, and has committed (subject to certain conditions) to lending you a specific amount.

In Portland’s competitive market, a pre-approval letter is non-negotiable for serious offers. Sellers and their agents want certainty—they want to know your financing won’t fall through mid-transaction. A strong pre-approval from a reputable local lender can make your offer significantly more attractive, sometimes even more so than a slightly higher price from a buyer with shaky financing.

From Offer to Keys: Navigating Oregon’s Unique Home Buying Process

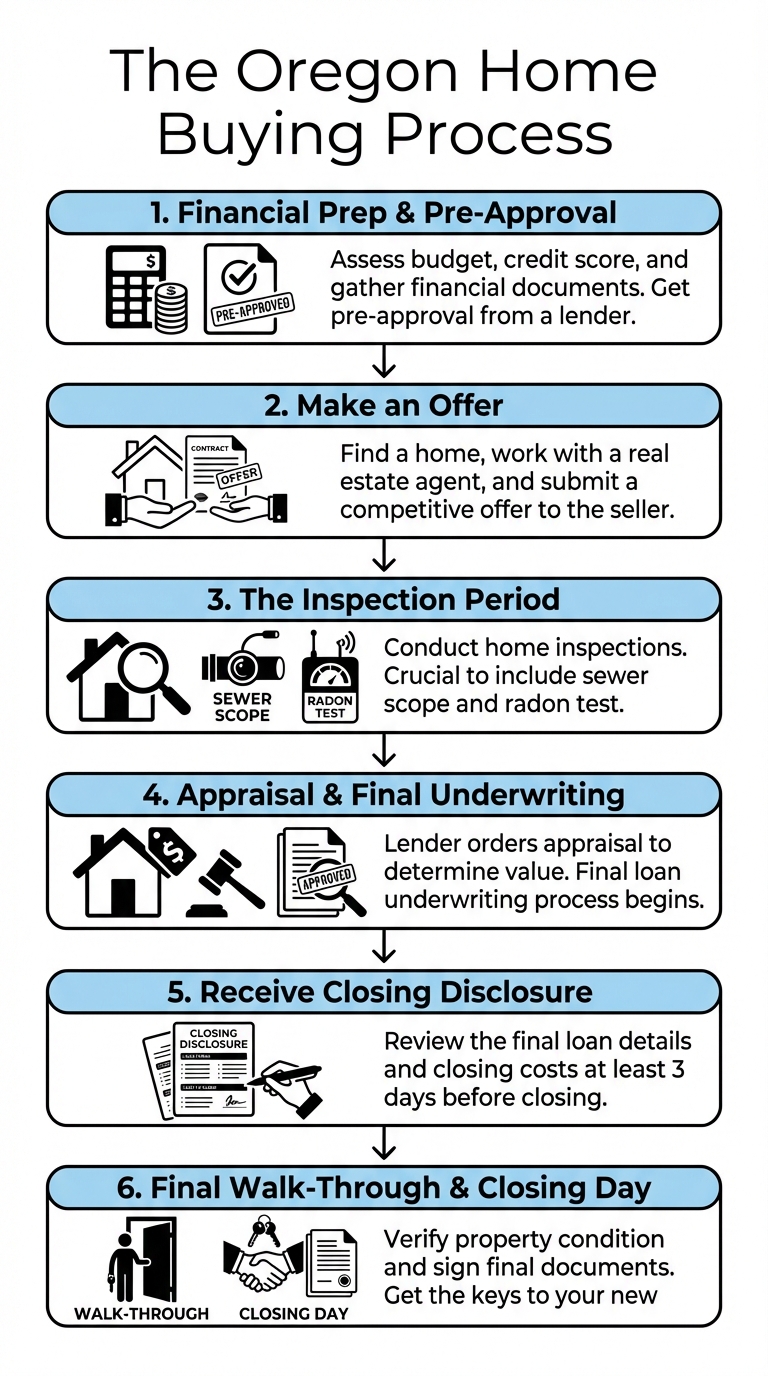

You’ve found a home you love, your finances are in order, and you’re ready to make an offer. Now comes the part that feels most overwhelming: the actual transaction process. Oregon’s home buying process has unique customs, legal requirements, and timelines that differ from other states. Let’s demystify each step.

Step 1: Agency & Representation—Whose Side Are They On?

In Oregon, real estate agents must clearly disclose whom they represent. When you work with a buyer’s agent, they have a fiduciary duty to represent your best interests—not the seller’s, not both parties equally, but yours. This relationship is formalized through agency disclosure forms and often a buyer representation agreement.

Your agent is your advocate, your negotiator, your guide through the paperwork jungle, and your strategic advisor. In a complex market like Portland, an experienced local agent who knows neighborhood nuances, understands Oregon’s disclosure laws, and has relationships with inspection professionals and lenders is invaluable.

Step 2: Making an Offer—The Art of the Deal

In Oregon, an offer to purchase a home is a legally binding contract. It’s not a casual expression of interest—once accepted, both parties have legal obligations. Your offer will include:

Sale Price: The amount you’re willing to pay. In competitive markets, this may be at, above, or (in a buyer’s market) below the asking price.

Earnest Money Deposit: Typically 1-3% of the sale price, held in escrow to demonstrate your serious intent. If the sale closes, this money applies toward your down payment. If you back out without a valid contingency, you may forfeit it.

Contingencies: Your Safety Nets

Contingencies are conditions that must be met for the sale to proceed. They’re your escape hatches if something goes wrong:

- Inspection Contingency: Allows you to conduct professional inspections and either negotiate repairs, request a price reduction, or walk away if major issues are discovered.

- Financing Contingency: Protects you if your loan falls through for reasons outside your control.

- Appraisal Contingency: Ensures the home appraises for at least the purchase price. If it appraises low, you can renegotiate or exit the contract.

In Portland’s competitive environment, some buyers waive contingencies to make their offers more attractive. This is risky—never waive an inspection contingency unless you’re prepared to accept the property “as-is” with potentially expensive hidden problems.

Step 3: Oregon’s Seller Disclosure Law—Knowledge Is Power (But Not Perfect)

Oregon law requires sellers of most residential properties to provide a Seller’s Property Disclosure Statement. This multi-page document requires sellers to disclose known material defects about the property—everything from roof condition to plumbing issues, structural problems to pest infestations.

Critical caveat: This disclosure is based on the seller’s actual knowledge. It’s not a warranty, and it’s not a substitute for professional inspections. Sellers can check “Don’t Know” for items they genuinely don’t know about. Your job is to verify everything through professional inspections, not just trust the seller’s disclosures.

Step 4: The Inspection Period—Your Due Diligence Power Move

This is arguably the most critical phase for protecting your investment. Portland’s housing stock includes many charming older homes with character—and sometimes with deferred maintenance. Essential inspections for Portland homes include:

General Home Inspection: A licensed inspector conducts a visual examination of the home’s structure, roof, foundation, electrical systems, plumbing, HVAC, and major appliances.

Sewer Scope Inspection: Critical for older Portland homes. A camera is inserted into the sewer line to check for tree root intrusion, breaks, or outdated materials (clay, orangeburg pipe). Sewer line repairs can cost $10,000-$30,000—this is not a place to skip inspection.

Radon Testing: Radon is a naturally occurring radioactive gas that can seep into homes through foundation cracks. Oregon has known radon risk areas, particularly in certain soil types. Testing is inexpensive and can identify a serious health hazard.

Underground Oil Tank Search: Many older Portland homes were heated with oil stored in underground tanks. If a tank wasn’t properly decommissioned or removed, it can leak and create significant environmental liability and cleanup costs. A specialized search involves reviewing records and sometimes using ground-penetrating radar.

Inspection findings give you leverage. You can:

- Request that the seller make repairs before closing

- Negotiate a price reduction to account for needed repairs

- Walk away if the issues are too severe (if your inspection contingency is in place)

Step 5: Understanding Oregon Property Taxes—The Measures 5 & 50 System

Oregon has a unique property tax system that often confuses newcomers. Thanks to Measures 5 and 50 (voter-approved initiatives), a property’s tax assessment can only increase by a maximum of 3% annually, regardless of the property’s actual market value.

Here’s why this matters: Two identical, side-by-side homes could have vastly different tax bills if one was last sold ten years ago and the other just sold yesterday. When you purchase a home, the property will be reassessed to its current market value for tax purposes.

Always review the current property tax bill, but understand it will change upon your purchase. Your lender will help you estimate the new tax bill, which affects your monthly payment and your debt-to-income ratio.

Step 6: From Appraisal to Closing—The Final Sprint

Once inspections are complete and any issues negotiated, the process moves to its final stages:

Appraisal: Your lender orders an independent appraisal to confirm the home’s value supports the loan amount. If the appraisal comes in low, you may need to renegotiate the price, bring extra cash to closing, or potentially exit via your appraisal contingency.

Final Loan Underwriting: Your loan application goes through final underwriting, where the lender verifies all documentation one last time. They may request additional paperwork or clarification.

Closing Disclosure: At least three business days before closing, you’ll receive your Closing Disclosure—a standardized form detailing your final loan terms and all closing costs. Review this carefully and compare it to your initial Loan Estimate. This three-day waiting period is mandated by the Consumer Financial Protection Bureau to ensure you have time to review and understand all terms before signing.

Closing Day: You’ll meet with an escrow officer (Oregon is an escrow state, not an attorney state for closings) to sign your final documents. You’ll wire or bring a cashier’s check for your down payment and closing costs. Once everything is signed and funds are verified, the deed is recorded, and you receive the keys to your new home.

The typical timeline from accepted offer to closing is 30-45 days, though this can vary based on financing complexity, inspection issues, and whether the seller needs time to find their next home.

Let’s Talk About What You’re Really Worried About

Buying a home—especially your first home—triggers a predictable set of anxieties. Let’s address them head-on with data and strategy, because fear thrives in the absence of information.

Fear #1: “What if I’m buying at the top of the market?”

This is perhaps the most common fear, and it’s understandable. Nobody wants to buy a home only to watch its value drop immediately.

Here’s the reality: Market timing is notoriously difficult, even for professional investors. The historical data for Portland shows that despite short-term fluctuations—including the 2008-2010 correction—home values have demonstrated a consistent long-term upward trajectory. The chart we examined earlier from the Federal Reserve clearly illustrates this decades-long appreciation trend.

The strategic shift: Instead of trying to time the market (which is essentially gambling), focus on two questions:

- Can you comfortably afford the monthly payments?

- Do you plan to stay in the home for at least 5-7 years?

If you answer yes to both, you’re positioned to weather short-term market fluctuations. Real estate is a long game, not a flip. Those who bought in Portland in 2006 (right before the crash) and held through the downturn have seen substantial appreciation. Those who panic-sold often locked in losses.

The worst time to buy is when you’re financially overextended or might need to sell within a year or two. The best time to buy is when you’re financially prepared and ready to commit to an area for the medium to long term.

Fear #2: “What if something major breaks right after I move in?”

The vision of a failed furnace in winter or a flooded basement shortly after closing haunts many first-time buyers. This fear is addressed through the inspection contingency and strategic preparation.

Mitigation strategies:

Thorough Inspections: This is your shield. A comprehensive general inspection plus specialized inspections (sewer scope, roof certification if needed, HVAC evaluation) provides a detailed picture of the home’s condition. You’re not looking for perfection—even new homes have issues—but you want to understand what needs attention now versus in the next 1-2 years versus in 5-10 years.

Budget for Maintenance: A common rule of thumb is to set aside 1-3% of your home’s value annually for maintenance and repairs. On a $550,000 home, that’s $5,500-$16,500 per year. Major systems like roofs, HVAC units, and water heaters have predictable lifespans. Your inspection report helps you anticipate these expenses.

Home Warranty (Optional): For peace of mind in the first year, many buyers purchase a home warranty that covers major systems and appliances. These typically cost $300-$600 annually with service call fees. They’re not perfect—they have coverage limits and exclusions—but they can cushion the blow of an unexpected major repair.

The inspection contingency exists precisely so you can make an informed decision. If the home has deferred maintenance that concerns you, negotiate repairs, request a price reduction, or walk away.

Fear #3: “The paperwork is overwhelming—what if I miss something critical?”

Real estate transactions generate mountains of paperwork, and the fear of signing something you don’t fully understand is legitimate.

Focus on the two most important documents:

Loan Estimate: Provided within three business days of your loan application, this standardized form details your loan terms, projected payments, and estimated closing costs. It’s designed by the CFPB to be clear and comparable across lenders.

Closing Disclosure: Provided at least three business days before closing, this finalizes all numbers and terms. Compare it line-by-line to your Loan Estimate. Any significant changes should be explained by your lender.

Your real estate agent and loan officer should walk you through every important document, explaining terms and answering questions. Don’t be embarrassed to ask for clarification—you’re making what’s likely the largest financial transaction of your life. There are no “dumb” questions when six figures are on the line.

Fear #4: “What if my offer isn’t competitive enough?”

In Portland’s market, multiple-offer situations still occur on well-priced homes in desirable neighborhoods. Here’s a real-world case study that illustrates how to compete effectively:

Scenario: A Southeast Portland Bungalow

A charming 1920s bungalow in a walkable Southeast Portland neighborhood hits the market at $525,000. Within three days, the seller receives three offers:

- Buyer A (The Strategic First-Timer): Offers $535,000 with a full pre-approval from a reputable local lender, includes a standard 10-day inspection contingency, and provides a personal letter expressing genuine connection to the neighborhood.

- Buyer B (The Uncertain Bidder): Offers $540,000 but only has a pre-qualification letter (not full pre-approval), creating uncertainty about financing.

- Buyer C (The Risky High-Roller): Offers $530,000 but waives the inspection contingency entirely—a risky move that could expose them to significant unforeseen costs.

The seller chooses Buyer A.

Despite not having the highest offer, Buyer A presented the least risk and highest certainty of closing. The full pre-approval demonstrated solid financing, the inspection contingency was reasonable (sellers understand buyers need to inspect), and the personal connection suggested a motivated buyer who would work through any issues that arose.

Key lesson: The strongest offer isn’t always the highest price—it’s the one that gives the seller the most confidence the deal will actually close. Your pre-approval, reasonable contingencies, flexible closing timeline, and professional presentation all matter.

Work with your agent to understand the seller’s priorities. Are they in a rush? Offer a quick closing. Do they need time to find their next home? Offer a rent-back period. Strategic thinking often beats throwing extra money at a property.

Final Thoughts

Buying your first home in Portland is challenging—there’s no sugarcoating that reality. The median price of $550,000 represents a significant financial commitment, and the market’s competitive nature means you need to bring your A-game.

But here’s what we’ve established throughout this guide:

You can navigate this market with the right preparation. Understanding current market conditions, neighborhood pricing dynamics, and historical trends transforms vague anxiety into strategic decision-making.

Financial readiness is your foundation. Managing your credit score, understanding your debt-to-income ratio, and leveraging Oregon’s specific assistance programs—the Oregon Bond Residential Loan Program and Portland’s Down Payment Assistance Loan (DPAL)—can bridge the affordability gap.

Oregon’s home buying process has unique elements—from agency representation to seller disclosures to the Measures 5 & 50 property tax system—but none of it is insurmountable when you understand what’s happening and why.

Strategic thinking beats emotional reactions. Whether you’re worrying about market timing, managing inspection negotiations, or competing in a multiple-offer scenario, knowledge and strategy consistently outperform gut-level reactions.

Most importantly: You don’t have to navigate this alone. Working with a knowledgeable local real estate professional who understands Portland’s neighborhoods, Oregon’s legal framework, and the current market dynamics transforms the process from overwhelming to manageable.

At GW Hartley IV, I specialize in guiding first-time buyers through the Portland market. I understand the assistance programs, the inspection red flags specific to Portland homes, and how to craft competitive offers that protect your interests while appealing to sellers.

Ready to take the next step? Let’s have a conversation about your specific situation, timeline, and goals. Whether you’re six months away from being ready or you want to start looking this weekend, I’m here to provide honest guidance tailored to your needs.

Ready to Make Your Portland Homeownership Dream a Reality?

Let’s discuss your unique situation and create a personalized strategy to get you into your first home.

References:

- Regional Multiple Listing Service (RMLS). (2024). Market Action Reports for the Portland Metro Area. Retrieved from https://www.rmlsweb.com/v2/public/marketstats.asp.

- Federal Reserve Bank of St. Louis. (2024). All-Transactions House Price Index for Portland-Vancouver-Hillsboro, OR-WA (ATNHPIUS38900Q). FRED, Federal Reserve Economic Data. Retrieved from https://fred.stlouisfed.org/series/ATNHPIUS38900Q.

- Oregon Metro. (2024). Urban growth boundary. Retrieved from https://www.oregonmetro.gov/urban-growth-boundary.

- Portland State University, Center for Real Estate. (2023). State of Housing in the Portland-Vancouver Metro Area Report. Retrieved from https://www.pdx.edu/real-estate/research-reports.

- U.S. Census Bureau. (2023). QuickFacts: Portland city, Oregon. Retrieved from https://www.census.gov/quickfacts/portlandcityoregon.

- National Association of Realtors. (2023). 2023 Profile of Home Buyers and Sellers. Retrieved from https://www.nar.realtor/research-and-statistics/research-reports/highlights-from-the-profile-of-home-buyers-and-sellers.

- Consumer Financial Protection Bureau (CFPB). (2022). What is a good credit score? Retrieved from https://www.consumerfinance.gov/ask-cfpb/what-is-a-good-credit-score-en-315/.

- Fannie Mae. (2023). Debt-to-Income (DTI) Ratios. Retrieved from https://selling-guide.fanniemae.com.

- Oregon Housing and Community Services (OHCS). (2024). Oregon Bond Residential Loan Program. Retrieved from https://www.oregon.gov/ohcs/homeownership/pages/homeownership-loan-program.aspx.

- Portland Housing Bureau. (2024). Down Payment Assistance Loan Program (DPAL). Retrieved from https://www.portland.gov/phb/dpal.

- Oregon Real Estate Agency (OREA). (2024). Buyer and Seller Resources. Retrieved from https://www.oregon.gov/rea/consumers/Pages/Consumer-Information.aspx.

- Oregon Health Authority. (2024). Radon Gas in Oregon. Retrieved from https://www.oregon.gov/oha/ph/healthyenvironments/radiationprotection/pages/radon.aspx.

- Consumer Financial Protection Bureau (CFPB). (2022). The 3-day rule: When do I get my Closing Disclosure? Retrieved from https://www.consumerfinance.gov/ask-cfpb/when-do-i-get-my-closing-disclosure-en-1985/.

- National Low Income Housing Coalition. (2023). Out of Reach 2023: The High Cost of Housing. Retrieved from https://nlihc.org/oor/oregon.

- U.S. Department of Housing and Urban Development (HUD). (n.d.). FHA Loans. Retrieved from https://www.hud.gov/buying/loans.

- U.S. Department of Veterans Affairs. (2024). VA Home Loan Types. Retrieved from https://www.va.gov/housing-assistance/home-loans/loan-types/.

- U.S. Department of Agriculture. (2024). Single Family Housing Guaranteed Loan Program. Retrieved from https://www.rd.usda.gov/programs-services/single-family-housing-programs/single-family-housing-guaranteed-loan-program.

- Oregon State Legislature. (2023). ORS 105.464 – Seller’s property disclosure statement. Retrieved from https://www.oregonlegislature.gov/bills_laws/ors/ors105.html.

- Oregon Department of Revenue. (n.d.). Property tax assessment and calculation. Retrieved from https://www.oregon.gov/dor/programs/property/pages/property-tax-assessment-and-calculation.aspx.